TL;DR

- Generative AI breaks the flat-rate seat. Variable inference cost flips SaaS economics: margin no longer scales with adoption but can shrink with it. Bessemer puts AI applications at 50–60% gross margins versus 80–90% for SaaS.

- Hybrid pricing is often the most practical pattern. A subscription base plus consumption overage (or prepaid credits with drawdown) can protect margin without scaring buyers away.

- The CFOs and CPOs succeeding in the next phase pick a monetization avenue (End Product, Value Booster, Add-on, or Super Tier), pick a pricing model that lets cost track value (Per Agent, Per Activity, Per Output, or Per Outcome), and build an operating stack, metering, billing, revenue recognition, and audit that supports hybrid pricing.

- Monetization is a coalition sport. The CFO, the CPO, and the CIO co-own the operating stack. Finance no longer ratifies what product was decided after the fact.

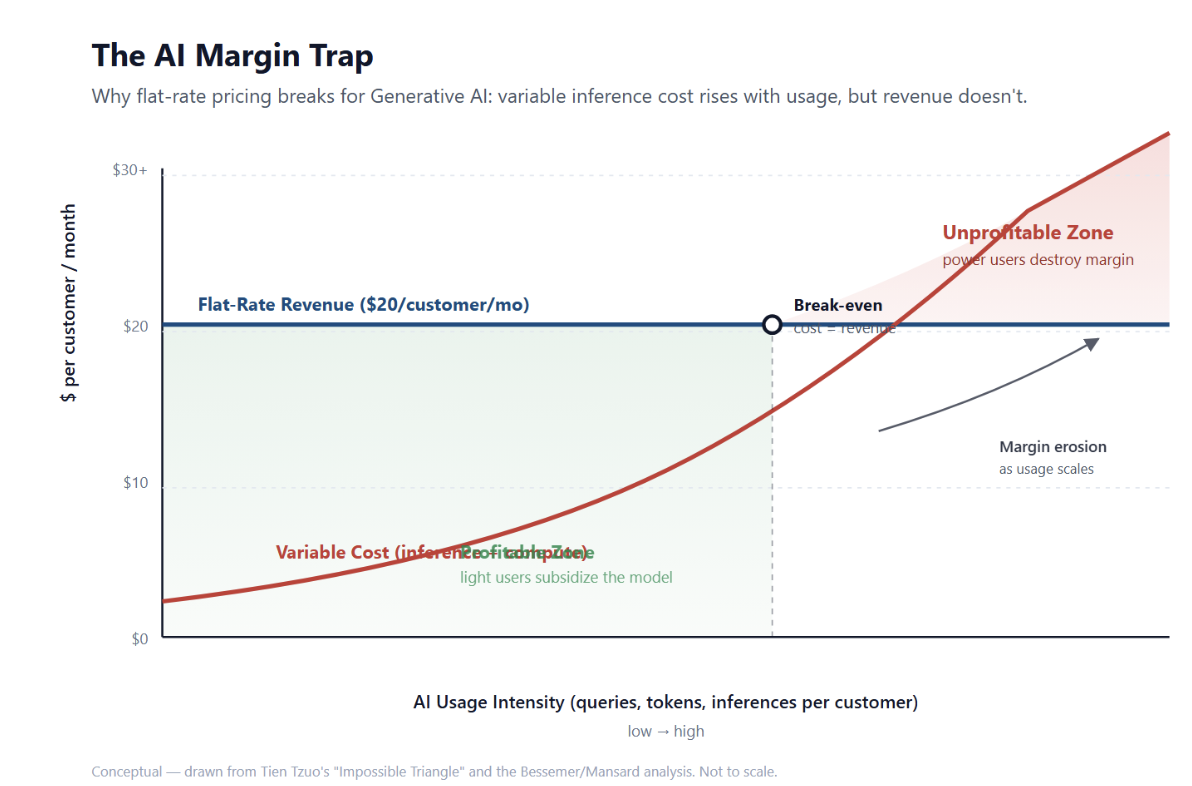

The AI Margin Trap (Why Flat-Rate Pricing Breaks for GenAI)

SaaS got rich on a simple identity: zero marginal cost. Once the software was built, the hundredth customer cost roughly the same to serve as the tenth. Gross margins expanded with adoption. The flat-rate subscription was the natural commercial expression of that economic reality.

GenAI doesn’t share this identity. Every query, every agent action, every generated artifact triggers a real, variable cost, including model inference, tokens consumed, vector retrieval, context-window expansion. CloudZero’s FinOps In The AI Era report (February 2026) found that 40% of surveyed companies now spend $10M+ per year on AI — and that mean Cloud Efficiency Rate has dropped 15 points across all segments (from 80% to 65%) as AI spending outpaces visibility into ROI. The cost is not a one-time investment but a recurring tax on usage.

That changes the shape of the margin curve. With flat-rate pricing, revenue per customer is a horizontal line. Inference cost per customer rises with adoption. The two lines cross. Past that crossover, every additional unit of customer engagement reduces gross margin. Bessemer puts the average gross margin for AI applications at 50–60%, versus 80–90% for traditional SaaS.

Look at how the companies actually shipping agentic AI have priced it. Salesforce charges $2 per conversation for Agentforce. Intercom charges $0.99 per resolution for Fin. Almost none have left agentic AI inside the existing flat-rate seat. Pricing follows the cost structure, but when the cost structure changes, pricing has to change with it.

CFOs already know what happens next. A finance system designed for monthly recurring revenue can’t, by itself, support pricing tied to per-conversation, per-resolution, or per-output economics. Monetizing AI is both a pricing decision and an operating-stack decision.

The Cost-Adoption-Value Triangle

Mansard’s research at the Zuora Subscribed Institute frames AI monetization as a balance among three forces: Cost, Adoption, and Value. Every monetization decision optimizes for one of the three, and the choice determines the trade-offs that the business has to live with.

Cost-oriented pricing

A cost-oriented pricing model sets price as a markup on the underlying inference cost, such as token-pass-through, cost-plus, or per-call billing tied to compute. The internal pitch writes itself: margin is preserved by construction.

The problem shows up in the customer’s wallet. Customers don’t buy compute. They buy the outcome that the compute produces. Pricing that exposes the cost mechanism caps willingness-to-pay at the cost itself, plus a thin markup. The seller leaves the value premium on the table, the premium that motivated the buyer to use the AI in the first place.

Cost-oriented pricing is appropriate when the product actually is an infrastructure layer (token APIs, embedding services). For application-layer AI, it underprices the offer.

Adoption-oriented pricing

Adoption-oriented pricing optimizes for getting the AI into the buyer’s hands quickly, flat-rate seats, all-you-can-eat tiers, and generous free allowances. This is the SaaS playbook applied without modification, and it works in the short term.

But in the medium term, it breaks. The companies that priced GenAI features as “free with your existing seat” in 2023 and 2024 are now reporting margin compression, throttled access, or quiet migrations to usage-based pricing for power users. The WSJ reported in October 2023 that GitHub’s Copilot business averaged a $20-per-user monthly loss, even as the product was a commercial success in adoption terms.

The right context for adoption-oriented pricing is a controlled launch window. As a steady-state model with variable AI cost underneath, it doesn’t hold up.

Value-oriented pricing

Value-oriented pricing aligns price with the unit of value that the AI delivers, including resolved tickets, drafted contracts, qualified leads, and predicted forecasts. This is the model that captures the economics buyers actually feel, and where most CFOs eventually land.

The challenge with value-oriented pricing is operational. The business has to meter the unit of value, attribute it to a customer, and recognize the revenue under ASC 606, even when the unit of value is something like “ticket resolved by AI without human intervention.” Zuora Revenue handles this last step.

Cost, Adoption, and Value are not a “choose one”. The strongest commercial outcomes blend cost-floor protection with adoption-friendly entry pricing and value-anchored upside. The next four steps build that blend.

Step 1: Choose Your Monetization Avenue

Before pricing, before packaging, before the operating stack, finance and product have to agree on what the AI is, commercially. Mansard’s analysis of 70+ companies identifies four monetization avenues, each with a different revenue shape.

- End Product (22% of offers). The AI is the product. Customers buy it directly, think of Jasper, Midjourney, and Cursor. Revenue scales with AI adoption and AI quality. Pricing is usually consumption-anchored or hybrid.

- Value Booster (33%). The AI deepens an existing product without being a separate SKU. Examples include Microsoft Copilot inside Office 365 (in its early phase), Notion AI inside Notion, and HubSpot’s AI assistants inside the CRM. Revenue scales with retention and tier upgrades, not direct AI usage.

- Add-on (27%). The AI is sold as a paid extension of the existing product, like with Asana Smart Goals, Salesforce Einstein, and Adobe Firefly Credits. Revenue is a discrete line item, attached to the existing customer relationship.

- Super Tier (18%). The AI is gated behind a higher-tier or “AI-Enabled” plan. ChatGPT Plus, Notion Plus, Linear Plus. Revenue scales with tier migration.

“AI has been a game-changer for us. We’ve been working on AI for years, integrating it into our products to automate tasks like bookkeeping. This allows us to offer an outcome-based pricing model rather than charging based on the number of users. It’s a shift away from the traditional pricing model, as we now focus on the outcomes our customers achieve with our solutions.” — Pascal Houillon, CEO, Cegid

The avenue choice is upstream of pricing. End Product economics support consumption pricing naturally. Add-on economics often work cleanest as a fixed-fee uplift. Super Tier is the cleanest path for businesses with a strong existing tiering motion. The wrong avenue forces the wrong pricing fight downstream.

Step 2: Choose Your Packaging Model

Once the avenue is set, packaging defines how the AI is presented commercially. Mansard’s packaging research shows that three patterns dominate:

- Good-Better-Best (57%). Three named tiers, each with a different level of AI access. This is the dominant pattern, and it works well when the AI’s value scales cleanly with feature breadth (more agents, more integrations, longer context windows in the higher tiers).

- Single Tier (24%). One offer, one price point. This option is rare but viable for focused products. It’s often a transitional state on the way to GBB once usage data accumulates.

- À la Carte (19%). AI features are priced individually, often atop a base subscription. Adobe Firefly’s credit packs are the cleanest example.

The packaging decision is where the bundle trap shows up. Lenny’s analysis of 44 AI companies found 59% bundle AI into existing packages, 23% sell it as an add-on, and 18% sell it standalone. Bundling is the path of least friction in the short term because customers see no price increase, and the sales team doesn’t have to renegotiate. It also offers the least pricing power. When inference cost rises, the seller has no mechanism to recover it without reopening the contract.

The strongest packaging strategies treat bundling as a customer-acquisition tactic for one quarter and a pricing-power liability the next. Packaging should evolve as adoption data and cost data become real.

Step 3: Choose Your Pricing Model

Pricing is where avenue meets cost. There are four canonical agentic pricing models, each captured in Mansard’s COMPASS Framework and explored in depth in Zuora’s AI pricing models guide.

- Per Agent. Customer pays per AI seat, i.e., one digital assistant, one license. This model is familiar to SaaS buyers, but it breaks down when a single agent processes thousands of variable-cost activities.

- Per Activity. Customer pays per call, per query, per workflow run. Salesforce Agentforce ($2/conversation) is the canonical example. This model aligns price with cost without exposing token economics to the buyer.

- Per Output. Customer pays per generated artifact — like an image, contract, email, or demand letter. Adobe Firefly’s credit packs and EvenUp’s per-demand-letter pricing both sit here.

- Per Outcome. Customer pays only when the AI delivers a defined business result, for example, Intercom Fin charges $0.99 per resolved ticket, Zendesk charges per autonomous resolution. The buyer transfers cost variance back to the seller, which means the seller had better understand its own unit economics.

Most production AI businesses converge on a hybrid: a subscription base for predictability, plus a consumption overage or prepaid credit pool that absorbs the variable cost. The hybrid pattern is what Genesys is building toward.

“To make the transition easier for our customers, we’re going for a token-based model. Customers can get bulk credits and use them across their seats or based on their AI engagements.” — Ramya Raj, VP & Global Head of Go-to-Customer Solutions, Genesys

The COMPASS Framework gives finance and product a shared decision tool for picking the model that fits the avenue, the packaging, and the cost structure. The full decision matrix lives in the AI pricing models guide, and the deeper agentic-pricing dive lives in pricing agentic AI.

Step 4: Build the Operating Stack

Pricing strategy without an operating stack is a slide deck. The operating stack is what turns a pricing decision into a billable, auditable, recognizable revenue stream.

Usage metering and mediation. Every consumption-based AI offer requires a rating engine that can count the unit of value (tokens, calls, resolutions, outputs) at production volume, attribute the count to a customer, and feed the count downstream to billing without manual reconciliation. Without this layer, hybrid pricing is theoretical.

Billing engine. Zuora Billing is the system most often called on to translate metered usage into invoiceable revenue. The billing engine carries the pricing logic, like base subscription, consumption tiers, prepaid credit drawdown, threshold-based overages, and produces the invoice that the customer actually pays.

Revenue recognition. Variable-outcome contracts complicate ASC 606. Revenue can’t be recognized on a flat schedule when the obligation is “resolve up to N tickets per month at $0.99 each.” Zuora Revenue handles this layer, recognizing revenue against actual fulfillment, maintaining the audit trail, and producing the disclosures public companies are required to file.

As a Chief Accounting Officer, I want to be able to say 'yes' to things that make sense commercially, so we have to be able to handle new business models, products, and offerings. With Zuora Revenue, we're able to be more agile to support the business so we can evolve with customer demands and go to market quickly.

Audit trail and governance. The Harris Poll research Zuora ran in March 2026 with 321 finance decision-makers, found 33% identify audit and explainability as the largest gap between AI promise and reality. The operating stack has to log the transaction and the AI decision behind it: which model, which version, which prompt, which output, which customer. Zuora’s certification under ISO/IEC 42001 (the AI management system standard) is the platform-level commitment to that governance layer.

The operating stack is what separates a pricing strategy that ships from one that gets revised under audit pressure six months later.

Step 5: Iterate, Measure, Evolve

Pricing for AI is not a one-time decision. The cost curve moves (frontier models get cheaper, customer usage grows, new model versions change inference economics). The competitive landscape moves (a competitor introduces outcome-based pricing and resets buyer expectations). The customer base moves (the cohort that signed in 2024 has different usage patterns from the cohort signing in 2026).

The CFOs who treat AI pricing as an annually revisited static decision lose ground. The ones who treat it as a continuous discipline with a quarterly cohort review, monthly margin-per-query monitoring, ongoing willingness-to-pay research, keep margin while the market moves.

Giving our customers immediate and accurate visibility into usage-based pricing is absolutely critical for an AI-powered integration platform like ours. With Zuora, we were live with usage metering in less than a month and able to provide instant visibility to usage data for our end customers.

The KPIs that matter for AI monetization are not the same as the KPIs that mattered for SaaS. Gross margin per query, gross margin per resolution, gross margin per active agent; these are the operational telemetry CFOs need. Adoption rate is still relevant, but it is now in tension with margin in a way it wasn’t under flat-rate pricing. Value-realized (the percentage of customers who hit the AI-driven outcome the offer promises) becomes a leading indicator of churn.

The operating stack should produce these KPIs continuously, not on a monthly close cycle. The monthly close is too late to course-correct.

The CFO, CPO, and CIO Coalition

AI monetization is one of the few commercial disciplines that requires three executive perspectives in lockstep. The CFO owns the margin and audit. The CPO owns the customer-facing offer. The CIO owns the technical infrastructure that makes the offer billable. None of the three can solve AI monetization alone.

The data confirms the coalition gap. Zuora’s Modern Finance Leader Report found:

- 97% of SaaS finance leaders say their current systems can’t fully support complex pricing (74% across the broader sample of finance leaders)

- 82% of SaaS leaders report operational challenges caused by fragmented order-to-cash ownership

- 71% of SaaS finance leaders report breakdowns or major operational struggles scaling order-to-cash to support usage-based pricing

- 95% of SaaS finance leaders say usage-based pricing makes forecasting harder (79% across the broader sample)

- 94% of SaaS finance leaders have rejected custom deals because order-to-cash couldn’t support them (68% across the broader sample)

The Harris Poll Zuora published in March 2026 (321 finance decision-makers, ±6.4% at 95% confidence) reinforces the gap on the AI side specifically. The trust-gap research found:

- 92% of finance teams now use AI in some form

- 87% see a gap between AI promise and AI reality

- 41% identify integration as the largest gap

- 33% identify audit and explainability as the largest gap

- 53% trust embedded AI more than standalone AI tools

- 43% are very confident AI works inside their existing financial controls and audit frameworks

“There’s no way we cannot be using the same technology that we have successfully implemented across our customer base. We had to walk the walk and become a lighthouse account ourselves.” — Todd E. McElhatton, COFO, Zuora

The coalition’s first job is to agree on what the operating stack must support before the product commits to a pricing model. That conversation is the one Zuora’s CFO + CIO leadership guide is designed to enable.

Common Pitfalls

The bundle trap. Bundling AI into the existing subscription is the easiest commercial decision in the short term and the hardest position to recover from in the medium term. Once buyers anchor on “AI is included,” repricing is a renegotiation, and not an upsell.

The seat-pricing comfort zone. Seat pricing is what the sales motion already knows how to sell. Defaulting to it for AI features because it fits the existing motion is a common margin-erosion mistake. Per-seat AI works when usage is predictable, and bounded copilots are used a few times a week. It breaks when usage is heavy and variable.

The cost-plus mistake. Pricing AI as a markup over inference cost ties the seller’s revenue to the buyer’s compute consumption rather than to the buyer’s outcomes. It also exposes the cost mechanism, capping willingness-to-pay at the underlying token economics. Cost-plus is a fallback model, not a strategic one.

Where to Start

The CFOs and CPOs who move first do three things in sequence.

- Quantify the margin exposure. Run the Margin Curve calculation on the AI-bearing portion of the existing offer. The output is a single number, the percentage of current AI revenue that turns negative gross margin past a defined usage threshold. That number is the budget for the rest of the work.

- Pick one pricing model to pilot. Hybrid (subscription base plus consumption overage) is the lowest-risk pilot for most businesses. Run it on one product line, one customer cohort, for two billing cycles. Measure margin-per-query and customer reaction.

- Validate the operating stack. Confirm that metering, billing, and revenue recognition can support the pilot end-to-end before scaling. ZOLL Data Systems implemented Zuora’s AI-Powered Collections in four weeks — a useful reference point for what stack-level change can look like when the foundation is already in place.

“These models may be complex, but they’re tameable with the right strategies and systems in place.” — David Crowell, Partner, Order to Cash, PwC

The practical sequence for finance and pricing leaders is the four-step playbook this guide laid out:

- Pick a monetization avenue (End Product, Value Booster, Add-on, or Super Tier);

- Pick the pricing model that fits that avenue and your AI’s cost structure (Per Agent, Per Activity, Per Output, or Per Outcome);

- Confirm the operating stack — metering, billing, revenue recognition, audit — actually supports the model end-to-end;

- Bring CFO, CPO, and CIO into the same decision, because none of the three can resolve the trade-offs alone.

For deeper strategic context, the AWS / PwC / Zuora AI Pricing Pivot whitepaper is the gated download.

For teams ready to evaluate the operating stack, the Zuora Billing demo is the next step.

For pricing leaders ready to compare the six pricing-model options in depth, the companion AI pricing models guide is the natural next read.

Frequently Asked Questions

1.

What is an AI monetization strategy?

AI monetization strategy is the set of decisions a company makes about how to convert AI capabilities into revenue, including which monetization avenue to pursue (End Product, Value Booster, Add-on, or Super Tier), how to package the offer (Single Tier, Good-Better-Best, or À la Carte), which pricing model to apply (Per Agent, Per Activity, Per Output, or Per Outcome), and what operating stack is required to support the chosen pricing model under variable inference cost.

2.

How is AI monetization different from SaaS monetization?

SaaS monetization assumes near-zero marginal cost — once the software is built, the next customer costs roughly the same to serve as the previous one. AI monetization has to account for variable inference cost, which means the margin can shrink with adoption rather than expand. Bessemer’s research puts AI applications at 50–60% gross margins compared with 80–90% for traditional SaaS. The pricing model has to track value or activity, not just access, to keep margin stable.

3.

How do you monetize AI without destroying margins?

A common pattern is hybrid pricing — a subscription base for predictability plus a consumption overage or prepaid credit pool that absorbs variable cost. Per-Activity pricing (charging per call, per query, or per workflow) and Per-Outcome pricing (charging per resolved ticket or per delivered result) both align price with cost. The operating stack — metering, billing, and revenue recognition — has to support the chosen model end-to-end before margin can be protected at scale.

4.

What are the four agentic AI pricing models?

Per Agent (price per AI license), Per Activity (price per call, query, or workflow run), Per Output (price per generated artifact), and Per Outcome (price per business result delivered). The COMPASS Framework, published by Zuora’s Subscribed Institute, maps these four models to the scope of the agent’s work and the level of attribution between agent action and business outcome. Most production AI businesses run hybrid models that combine two or more.

5.

Should AI features be bundled or sold as add-ons?

Bundling lowers acquisition friction and is the most common short-term path — Lenny’s analysis of 44 AI companies found 59% bundle AI into existing packages. Add-on pricing (23% of companies) preserves pricing power and gives the seller a mechanism to capture additional value as adoption grows. Standalone AI products (18%) command the highest pricing power but require the most commercial muscle to launch. The right answer depends on the avenue (Add-on works for Add-on Avenue; bundling works for Value Booster) and the cost structure of the AI itself.

6.

How do CFOs measure AI ROI?

Gross margin per query, gross margin per resolution, and gross margin per active agent are the operational telemetry that matter for AI monetization specifically. Adoption rate remains relevant but is now in tension with the margin under variable-cost pricing. Value-realized — the percentage of customers who hit the AI-driven outcome the offer promises — is a leading indicator of churn. The Modern Finance Leader Report found 97% of SaaS finance leaders say their current systems can’t fully support complex pricing (74% across the broader sample of finance leaders), which is why the operating stack matters as much as the pricing model.

7.

What systems are needed to support dynamic AI pricing?

Four layers are stacked in sequence. A usage metering and mediation layer counts the unit of value at production volume. A billing engine translates metered usage into invoiceable revenue (Zuora Billing is the most common choice). A revenue recognition layer handles ASC 606 for variable-outcome contracts (Zuora Revenue). An audit and governance layer logs the AI decision behind each transaction. Zuora’s certification under ISO/IEC 42001 is the platform-level commitment to the governance layer.