AI Agents for Accounts Receivable: The New AR Operating Model

An AI agent for accounts receivable is software that can reason over invoices, payments, customer history, and collections workflows to recommend or execute AR actions under finance controls. The safest AR AI runs on trusted billing data, respects approval policies, and produces audit-ready explanations for every action.

Leveraging the power of AI, Zuora Collections demonstrates a deep understanding of the evolving needs of subscription businesses.

The agentic-AR competitive arena is forming right now

A new group of emerging vendors is trying to define the next wave of AI-led AR operations. Their positioning often emphasizes faster execution, lighter workflows, and more autonomous handling of collections or exception-management tasks.

Zuora’s current position is better framed as AI-powered, governed AR workflows embedded in the finance system of record. The strongest public proof supports human-in-the-loop automation, permissions, auditability, and finance-grade controls rather than a public commitment to fully autonomous AR agents acting without approval.

Agentic AR is an emerging category. Many finance teams are exploring how AI can move from insight and prioritization into more operational execution, but maturity, deployment patterns, and buyer readiness still vary significantly by company size, controls environment, and systems architecture.

When evaluating agentic AR platforms, ask four practical questions: Does the platform operate on current billing and AR data? Does it support finance-grade permissions and audit trails? Can it work within controlled approval paths? And can it fit enterprise requirements for compliance, reporting, and systems-of-record integrity?

- Does the platform operate on current billing and AR data?

- Does it support finance-grade permissions and audit trails?

- Can it work within controlled approval paths and fit enterprise requirements for compliance, reporting, and systems-of-record integrity?

The technology shift is both real and consequential. The trust gap exists and is operationally limiting. The platforms that earn finance teams’ trust will be the ones whose agents run on clean billing data and operate within audit-defensible controls.

What Is an AI Agent for Accounts Receivable?

An AI agent for accounts receivable is software that can reason over invoices, payments, customer history, and collections workflows to recommend or execute AR actions under finance controls. It is distinct from rule-based AR automation, which executes programmed rules, and from AI-powered AR, which augments humans with predictions, drafts, and suggested actions.

The evaluation question is how much action the system can safely take, what approval paths govern those actions, and whether each decision can be audited.

AR Automation vs AI-Powered AR vs Agentic AR: Terminology Disambiguation

Three distinct categories that get conflated in vendor marketing.

- AR Automation (rule-based / RPA). Executes programmed rules. When invoice X reaches Y days overdue, send template Z. When payment matches invoice within tolerance, post and clear. Mature and well-deployed for repeatable cases.

- AI-Powered AR (predictive + classification + suggestion). Augments humans with predictions, classifications, and suggestions. AI scores accounts; humans confirm priorities. AI drafts outreach; humans confirm before sending. AI proposes a match for ambiguous payment; humans confirm before posting. Zuora’s current public position is better framed as AI-powered, governed AR workflows embedded in the finance system of record.

- Agentic AR (autonomous reasoning + action). An emerging category in which AI moves from insight and prioritization toward more operational execution. Maturity, deployment patterns, and buyer readiness still vary significantly by company size, controls environment, and systems architecture.

The conflation matters because vendor evaluations get noisy when “agentic” is used to describe what is actually AI-powered AR with confirmation steps. The substance question, i.e., does it actually act, or does it suggest and require confirmation, separates the categories.

Why “Agentic” Is Different

Autonomous reasoning plus action is a different capability from rule-based automation, even when the rules are sophisticated. A rules engine can express “if remittance advice contains invoice numbers I-3847, I-3848, I-3849, and the payment amount equals the sum of those invoices, post the multi-invoice match.” It can’t express “if the remittance advice is a PDF with handwritten annotations that combine three invoice numbers in formats the customer has used inconsistently in past payments, parse the document, infer the intended split, propose the match.” That is the capability shift the category is trying to define.

The shift matters operationally because the long tail of AR edge cases is too varied for rules to enumerate. The cases where rules fail are often the cases that consume the most AR Operations time. In finance-grade deployments, AI assistance should support those workflows with clear controls, approvals, and exception handling.

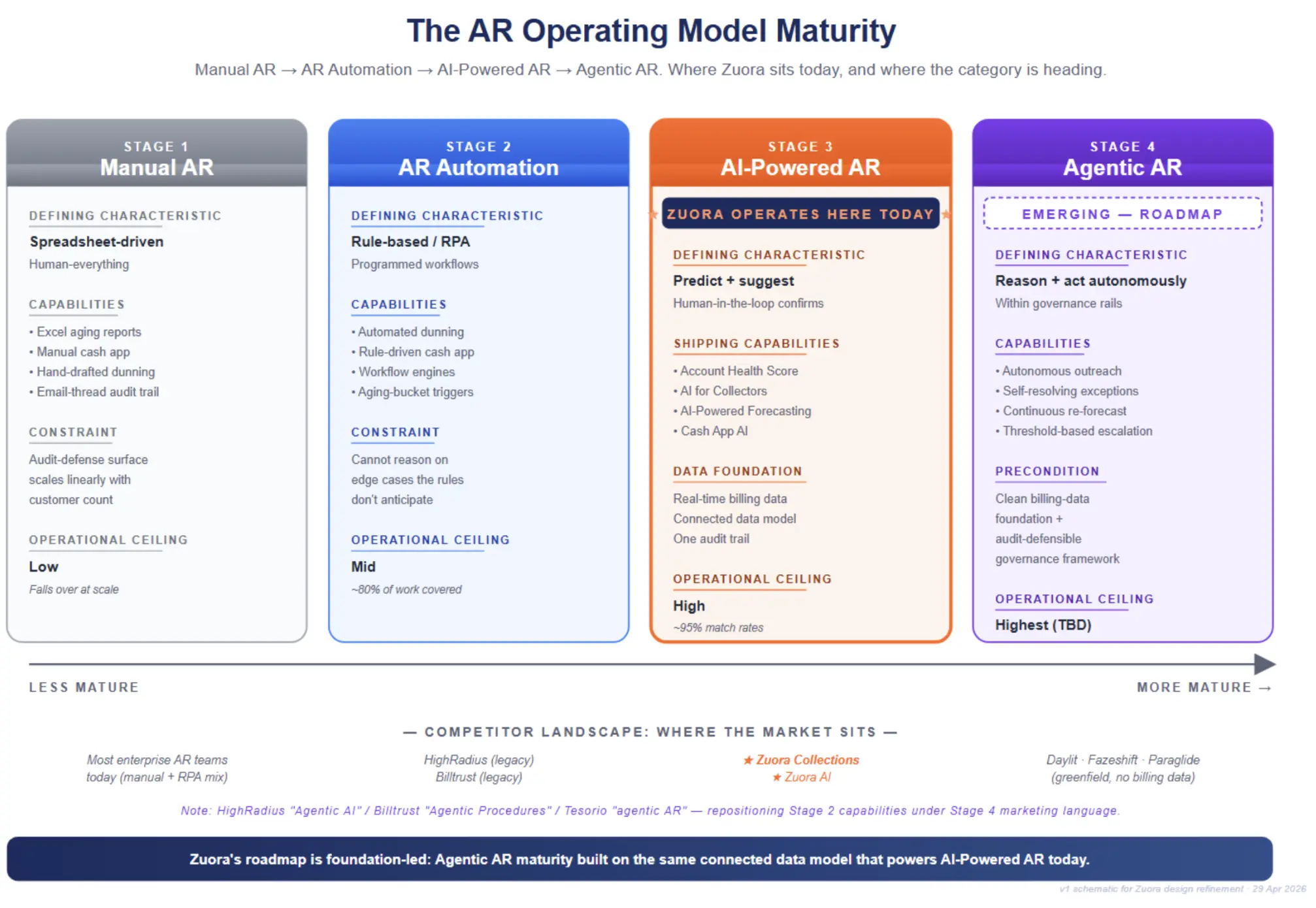

The AR Operating Model Maturity

The shift from Manual AR through Agentic AR is best understood as an operating-model maturity progression. Many finance teams span multiple stages at the same time, depending on workflow, controls environment, and systems architecture. The visual below shows the four stages with capability examples and platform positioning.

Stage 1 — Manual AR

Spreadsheet-driven, human-everything. The collections team manages aging in Excel, drafts outreach by hand, and matches cash by sorting and filtering. Any workflow still operating this way creates more manual effort, more audit-defense surface, and a lower operational ceiling at portfolio scale.

Stage 2 — AR Automation (RPA / Rule-Based)

Workflow engines, dunning automation, and rule-driven cash application. This model is mature and effective for deterministic AR work, but constrained by what rules can express for long-tail edge cases.

Stage 3 — AI-Powered AR

Predictive scoring, classification, and AI-assisted suggestion engines with human-in-the-loop confirmation. Zuora Collections helps teams automate follow-up, prioritize accounts, forecast collections outcomes, and manage collection activity in one workflow. Its AI-generated insights and health scores help teams identify high-risk accounts based on payment behavior, engagement patterns, and risk indicators. Collector dashboards and AR aging views help teams monitor overdue accounts, payment status, risk signals, and collection activity.

Stage 4 — Agentic AR

The emerging category. Agentic AR is the operating model in which AI takes action within governance rails rather than only suggesting actions for a human to confirm. The category is emerging across the AR vendor landscape. Public Zuora capabilities sit at Stage 3 (AI-powered AR), with capability evolution informed by the same connected data foundation, governance framework, audit trail, and human-in-the-loop control as the Stage 3 features already deployed.

What AI Agents in AR Actually Do

Beyond the abstract definition, the operational substance of an AI agent in AR is captured by what it actually does day-to-day.

Account Scoring and Prioritization

Prioritization should reflect more than the initial worklist. A composite priority model can combine days outstanding with customer value, payment behavior, dispute context, and strategic account context. In Zuora Collections, AI-generated insights and health scores help teams segment and prioritize accounts based on payment behavior, engagement patterns, and risk indicators.

Drafting Outreach With Context

The agent pulls customer context from the CRM, the billing system, and customer-success signals before drafting outreach. The reminder for a strategic account, 30 days late, references the open opportunity that the account has in negotiation. The reminder for a long-tail customer 60 days late references the auto-pay enrollment offer that would resolve the recurring failure pattern. Context-aware drafting is the difference between collections that build trust and collections that erode it.

Cash Application Matching for Edge Cases

Rules-based matching can handle many clean payments, while AI-assisted matching is useful for edge cases such as multi-invoice remittances, short-pays, ambiguous references, and partial payments.

For each, the system runs a similar assistance loop. It reads remittance advice, cross-references payment history and open invoices, and identifies likely matches for review through configured workflows. Zuora supports cash application with capabilities such as smart auto-match, remittance capture, OCR, advanced matching, and apply-and-post workflows, with controls shaped by entitlement, configuration, and approval paths.

The operational shift: a multi-minute research task for the human collector becomes a quick confirmation step.

Dispute Analysis and Routing

Customer replies fall into a few patterns: routine acknowledgment, payment promise, dispute indication, and frustration. Smart collections workflows classify each reply and route it accordingly — routine acknowledgments toward auto-closeout under approval controls, disputes to the appropriate human owner with full context (CRM, billing, recent touchpoints), and frustration signals to the account team for an early-warning touch. AI can assist with classifying inbound replies so routing keeps pace with volume.

Forecasting and Anomaly Detection

Continuous re-forecasting as collections actions land. The agent updates the cash-inflow model when payments post, when promises-to-pay come in, when disputes open, and when customer-success churn flags trigger. At-risk accounts get flagged before aging; aging-distribution shifts get flagged before they show up in the monthly close.

The Market Today: Who is Building Agentic AR

The landscape is still forming. Each vendor should be evaluated by what the workflow can actually do, what data it operates on, and how it handles controls, approvals, audit trails, and enterprise finance requirements.

New Entrants — YC-Backed Greenfield AI Agents

A new group of emerging vendors is trying to define the next wave of AI-led AR operations. Their positioning often emphasizes faster execution, lighter workflows, and more autonomous handling of collections or exception-management tasks. Buyers should evaluate actual workflow autonomy, data access, governance controls, and current enterprise capabilities rather than the category label.

When evaluating these tools, ask whether the platform operates on current invoice, payment, collection, and customer-context data, or whether it depends on periodic exports and reconciliation. The fresher and more complete the data, the more useful the prioritized workflow can be.

Incumbent Repositioning: Established AR Platforms Adopting Agentic Language

Established AR vendors are positioning existing capabilities alongside or under “agentic” framing. Public examples include HighRadius’s “Agentic AI” thought-leadership program, Billtrust’s “Agentic Procedures” branding, and Tesorio’s “agentic AR experience” content series.

When evaluating agentic AR platforms, ask four practical questions: Does the platform operate on current billing and AR data? Does it support finance-grade permissions and audit trails? Can it work within controlled approval paths? And can it fit enterprise requirements for compliance, reporting, and systems-of-record integrity?

Platform-Led Approach: Agentic AI Built on Connected Data

The Connected AR Automation Platform model is a different starting point. When evaluating agentic AR platforms, ask whether the workflow operates on current billing, collections, cash application, and AR accounting data, and whether it preserves finance-grade permissions, approvals, and audit trails.

Zuora’s current position is better framed as AI-powered, governed AR workflows embedded in the finance system of record, with capabilities that include:

- Account health and risk insights — AI-generated insights and health scores that help teams segment and prioritize accounts based on payment behavior, engagement patterns, and risk indicators

- AI for Collectors — AI-drafted outreach with collector review and AI-assisted handling of inbound customer replies

- AI-powered cash forecasting — forecasting support that helps teams understand expected collections outcomes

- Cash application capabilities — smart auto-match, apply and post, remittance capture, OCR, and advanced matching, subject to entitlement, configuration, and approval controls

Fuller autonomous agentic AR is an emerging category. Zuora’s capability evolution sits on this same connected data foundation, governance framework, audit trail, and human-in-the-loop control as the AI-powered features already deployed, with future roadmap direction subject to PMM/Product publication.

Why Agentic AR Works Only When Grounded in Billing Data

The strategic differentiation of the platform-led approach is the data foundation. Autonomous agents reason against the data they’re given. Bad data plus autonomous reasoning produces errors at machine speed.

The Garbage-In, Garbage-Out Problem for Autonomous Agents

Rule-based automation fails predictably when the data is bad. The rule fires or doesn’t, the exception queue gets longer, and the human notices the operational backup. Autonomous agents fail differently. They reason against the bad data, reach confident-looking conclusions, and act on those conclusions. The audit trail looks clean, but the underlying reasoning is wrong. The errors compound at the speed of automation.

Why Bolting Agentic AI Onto Legacy AR Amplifies Errors

When evaluating agentic AR platforms, ask whether the workflow operates on current billing and AR data, whether it supports finance-grade permissions and audit trails, whether it can work within controlled approval paths, and whether it fits enterprise requirements for compliance, reporting, and systems-of-record integrity.

The Billing System of Record as the Necessary Foundation

The connected architecture pattern matters because billing, collections, cash application, and AR accounting workflows can preserve shared invoice and payment context. When evaluating agentic AR platforms, ask whether the workflow operates on current billing and AR data, supports controlled approval paths, and preserves audit trails for disputes, amendments, and customer-context signals.

Agentic AI Safety and Governance for Finance

The trust gap is the largest barrier to agentic-AR adoption in finance, and Zuora-commissioned Harris Poll research (March 2026, 321 finance and accounting decision makers, ±6.4% precision at 95% confidence) maps it specifically.

The Trust Gap Is Real

Per the Zuora-Harris Poll AI in Finance research:

- 92% of finance and accounting decision makers say their finance teams are using AI tools.

- Only 28% are seeing a measurable financial impact from AI investment.

- 87% say there are gaps between AI promise and reality.

- Only 43% are very confident their AI tools operate within their existing financial controls and audit frameworks; 46% are somewhat confident; 11% are not confident.

- 91% have concerns about using AI for core financial processes.

- Top concerns: cybersecurity and data privacy (45%), lack of appropriate human oversight (38%), data quality and reliability (36%).

The data tells a consistent story. AI usage is widespread; financial impact lags; trust in controls compliance is partial; concerns are near-universal. The trust gap isn’t an abstract objection to agentic AI; it’s a specific operational concern about controls, oversight, and data integrity.

Audit Trails for Agent Actions

Each agent’s decision must be logged with full context. A defensible log captures:

- Agent identifier — which agent took the action

- Timestamp — when the action occurred

- Reasoning path — what data and rules the agent used to decide

- Action taken — the specific output (post, send, escalate, etc.)

- Exception handling — what triggered any deviation from default behavior

- Escalation trigger — what conditions (if any) routed the action to a human

The trail has to be queryable by the controller and defensible to an external auditor. Agents that can’t produce this audit trail aren’t deployable in regulated finance environments, regardless of their capability claims.

Human-in-the-Loop Checkpoints

The default should be human-in-the-loop on high-stakes actions, not human-out-of-the-loop autonomy. A typical threshold-based escalation model might look like:

- Write-offs above a defined dollar amount route to controller approval before posting

- Service-tier impact decisions route to the account-team owner for sign-off

- Dispute resolutions involving credit memos route to Finance approval

Inside the threshold envelope, the agent operates autonomously. Outside it, humans enter the workflow at the points where governance demands they do.

Role-Based Access and Approval Flows

Agents inherit role-based permissions from the platform’s existing access-control model. The agent that can post journal entries inherits the controller-role permissions; the agent that can update customer master data inherits the AR Operations Manager permissions. Approval flows mirror the human approval flows the team already uses. The pattern keeps controls aligned with the existing governance framework rather than introducing new control surfaces.

ASC 606 Compliance With Autonomous Actions

Agentic AR actions that touch write-offs, payment application, revenue impacts, or journal entries need to be governed by the same accounting policies, approvals, and audit trails as the underlying finance process. ASC 606 alignment is not automatic — it depends on revenue policies, controls, audit trail, exception handling, and how the agent’s actions are wired into the existing accounting system of record.

The architectural distinction worth evaluating is whether the agent operates on the same data model as Zuora Revenue, where agent actions can be governed by the controls already in place, or on exported data, where the integration team takes on the work of keeping those controls aligned.

Buyers should verify how each vendor supports revenue-recognition controls, multi-entity, multi-currency, and exception handling before deployment.

Why Embedded AI Is Trusted More

Finance and accounting decision makers were asked which AI delivery model they would trust most. The Zuora-Harris Poll research found a clear hierarchy:

- AI features embedded in existing solutions — 53%

- Custom AI built by the organization itself — 25%

- AI-native solutions — 13%

The trust-gap data aligns with the architectural argument. Embedded AI inherits the platform’s existing controls, audit trail, and role-based access framework. That inheritance is the precondition for agent actions to be defensible.

How to Evaluate AI Agents for AR

Five evaluation criteria that should structure any vendor shortlist.

Substance Check: Does It Actually Act, or Just Suggest?

The disambiguation matters. Vendors using “agentic” language for AI-powered features that still require per-action human confirmation are mis-categorizing the capability. Two demo questions separate the two cases:

- Does the agent send the dunning email autonomously, or does the collector confirm before sending?

- Does the agent post the cash-application match, or propose it for confirmation?

AI-powered AR is a real and useful capability. It just isn’t agentic AR, and vendor framing should reflect the difference.

Integration Depth: Real-Time Billing Data or Nightly Export?

This is the architectural test. Pose a specific hypothetical to the vendor: an invoice is amended at 2:17 pm. When is the agent reasoning against the amended state?

The practical evaluation question is whether the workflow operates on current invoice, payment, collection, and customer-context data, or whether it depends on periodic exports and reconciliation. The fresher and more complete the data, the more useful the prioritized workflow can be.

Audit and Governance: Can You Defend Its Actions to Your Auditor?

This is the controls test. Per the Harris Poll research, “ability to audit or explain AI-driven results across systems” was named by 33% of decision makers as among the biggest gaps between AI promise and reality. Agents that can’t produce defensible audit trails fail the controls test, regardless of operational capability.

Roadmap Alignment: Does It Scale to ASC 606, Multi-Entity, FX?

Connected finance platforms can make ASC 606 workflows easier by keeping billing, cash application, and downstream accounting data aligned. But compliance still depends on policy design, approvals, audit trails, exception handling, and revenue controls. Architecture helps, but it does not replace accounting governance.

Trust-Gap Mitigation: Does It Provide the Human-in-the-Loop Checkpoints That Finance Leaders Identify as the Precondition for Trust?

The Harris Poll data identifies “lack of appropriate human oversight” as a top-three concern (38%) in AI for core financial processes. The agents that earn finance leaders’ trust will be the ones that build human-in-the-loop checkpoints into the default workflow rather than positioning autonomy as the headline feature.

Connecting to AI Monetization: The CFO/CPO Bridge

The cross-cluster strategic linkage. CFOs and Chief Pricing Officers often hold both decisions in parallel: buying agentic AI for AR operations while their own teams are pricing the agentic AI products they ship to market.

Buying Agentic AI for AR Ops While Selling Agentic AI Products

The pattern is now common in the SaaS economy. The Finance and Pricing leadership of an AI-shipping company is typically the same leadership making AI-tooling decisions for the company’s own AR function. Both decisions face the same trust-gap dynamics: customers (in the sell-side conversation) are the same finance leaders (in the buy-side conversation), with the same concerns about controls, oversight, and data integrity.

Two Frameworks Anchor Both Sides of the Bridge

Two published frameworks apply directly to both sides of the bridge: evaluating agentic AR vendors as a buyer, and pricing the agentic AI products that a finance team’s own company ships.

The Impossible Triangle

The framework: Cost-to-Serve × Customer Adoption × Value Delivered. Most agentic-AI offerings fail to balance more than two of the three corners simultaneously.

Applied to agentic AR vendor evaluation, the three corners map to:

- Cost-to-Serve. The inference, integration, and audit-defense costs of running autonomous agents on customer billing data.

- Customer Adoption. Whether the finance team will actually trust the agent enough to deploy it operationally.

- Value Delivered. Whether the agent’s actions produce measurable gains in cash velocity, retention, or audit-defense surface.

A vendor strong on autonomous-reasoning UX but weak on integration architecture is failing the Cost-to-Serve corner. A vendor strong on capability but weak on governance is failing Customer Adoption. The Impossible Triangle gives the buyer a structural way to spot where an agentic-AR offering will run out of runway.

The COMPASS Framework

The framework: Scope of Work × Level of Attribution maps to the pricing model that fits, drawn from four options:

- Per Agent

- Per Activity

- Per Output

- Per Outcome

The framework matters on both sides of the bridge. On the buying side, it explains why agentic-AR vendor pricing is varying so widely right now: different vendors are positioning at different points on the COMPASS map, and like-for-like comparisons are harder than they look. On the selling side, it gives finance and pricing leaders the structure to think through the agentic-AI products their own company is bringing to market.

How to Price the Agentic AI You Ship

The complementary discipline is on the sell side. Pricing models for agentic AI products face new challenges that traditional SaaS pricing wasn’t built for: outcome-based vs subscription, per-event vs per-user, hybrid models that blend both. Our companion guide on agentic AI pricing covers the sell-side conversation in depth, including the practical application of the Impossible Triangle and COMPASS frameworks.

The cross-cluster bridge applies to both sides of finance leadership. The same dynamics shaping how teams evaluate agentic-AR vendors as buyers — data quality, AI substance over marketing, and governance frameworks that let AI capabilities operate inside finance controls — are shaping how their own companies price the agentic-AI products they ship.

The AR-buying decision and the AI-product-pricing decision both depend on current data, AI substance over marketing, and governance frameworks that let AI capabilities operate inside finance controls.

How Zuora Positions on Agentic AR

The architectural commitment matters more than the marketing claim. Zuora’s current position is better framed as AI-powered, governed AR workflows embedded in the finance system of record, with public proof for human-in-the-loop automation, permissions, auditability, and finance-grade controls.

Zuora Collections AI Features Already Shipping

Four named capabilities live today inside Zuora Collections, all operating on the same data model as the billing system of record:

- Account Health Score. Composite priority score combining aging, customer value, payment-behavior risk, and customer-success signals.

- AI for Collectors. Account scoring, AI-drafted outreach with collector review, and AI-assisted handling of inbound customer replies. The operational substance behind the AI-Powered AR experience.

- AI-Powered Forecasting. Continuous cash-inflow modeling on real-time AR data.

- Cash application capabilities. Smart auto-match, remittance capture, OCR, advanced matching, and apply-and-post workflows for cash-application operations.

These capabilities are best framed as governed, human-in-the-loop AR workflows that preserve permissions, auditability, approval paths, and finance-grade controls.

Zuora AI as the Platform-Level Commitment

Zuora AI is the platform-level program within which the Collections capabilities sit. The platform commitment is to embed AI within the existing finance system of record, where it inherits the data model, the governance framework, and the audit-defensible workflow logging that the platform already provides. Per the trust-gap research, this is the architectural pattern 53% of finance leaders trust most.

Governed Evolution Toward Agentic AR

Zuora’s current position is better framed as AI-powered, governed AR workflows embedded in the finance system of record. The strongest public proof supports human-in-the-loop automation, permissions, auditability, and finance-grade controls rather than a public commitment to fully autonomous AR agents acting without approval.

Get the Foundation Right First

The near-term opportunity in agentic AR is not to remove finance from the loop. It is to reduce manual work, speed up routine decisions, and give teams governed AI assistance inside systems they can audit and control. For finance leaders, the question is less whether autonomy is coming and more which parts of AR can be safely automated first.

For CFOs evaluating the category, four practical questions structure the work.

- Data foundation. Confirm whether the platform operates on current billing and AR data.

- Controls. Confirm finance-grade permissions, approval paths, audit trails, and exception handling.

- Enterprise fit. Confirm requirements for compliance, reporting, multi-entity operations, currencies, and systems-of-record integrity.

Ready to evaluate agentic AR for the modern CFO seat?

Watch a demo of Zuora Collections

Read the full Zuora-Harris Poll AI in Finance trust-gap research

FAQs

1.

What is an AI agent for accounts receivable?

An AI agent for accounts receivable is software that can reason over invoices, payments, customer history, and collections workflows to recommend or execute AR actions under finance controls. The safest AR AI runs on trusted billing data, respects approval policies, and produces audit-ready explanations for every action.

2.

How is agentic AI different from AR automation?

AR automation executes programmed rules. Agentic AI is an emerging model that can reason over customer context, payment behavior, and open-invoice data to recommend or execute next actions under finance controls. The two can coexist: rules handle deterministic patterns, while AI assistance supports workflows where context matters.

3.

What is the difference between AI-powered AR and agentic AR?

AI-powered AR augments humans with scoring, drafts, classifications, forecasts, and suggested matches. Agentic AR is the emerging category where AI moves from insight and prioritization into more operational execution under finance controls. Zuora’s current position is better framed as AI-powered, governed AR workflows embedded in the finance system of record.

4.

Are AI agents safe for finance teams?

AI agents are safer for finance teams when they operate on trusted billing data, respect approval policies, preserve role-based access controls, and produce audit-ready explanations. Per Zuora-commissioned Harris Poll research (March 2026, 321 finance and accounting decision makers), only 43% of finance leaders are very confident their AI tools operate within existing financial controls and audit frameworks.

5.

How do AI agents handle ASC 606 compliance?

Connected finance platforms can make ASC 606 workflows easier by keeping billing, cash application, and downstream accounting data aligned. But compliance still depends on policy design, approvals, audit trails, exception handling, and revenue controls. Architecture helps, but it does not replace accounting governance.

6.

Should I choose a dedicated AR AI agent or a billing-platform AI?

When evaluating agentic AR platforms, ask four practical questions: Does the platform operate on current billing and AR data? Does it support finance-grade permissions and audit trails? Can it work within controlled approval paths? And can it fit enterprise requirements for compliance, reporting, and systems-of-record integrity?

7.

How do I evaluate whether an AI agent has the data foundation to be safe?

Per Zuora-Harris Poll research, 53% of finance and accounting decision makers would trust AI features embedded in existing solutions most, compared to 25% trust in custom-built AI and 13% in AI-native solutions. The trust-gap data favors the embedded approach. The architectural test is whether the AI reasons on real-time data from the system of record, with audit-defensible governance. Where the answer is yes, the data foundation supports trustworthy outcomes; where it is no, the AR team’s operational outcomes will reflect the data foundation gap.

8.

What features should I look for in an AI agent for AR?

Enterprise-grade AR AI should support current billing and AR context, finance-grade permissions, controlled approval paths, audit trails, exception handling, reporting, and systems-of-record integrity. Buyers should also confirm which compliance, multi-entity, currency, and ERP workflows are supported today versus planned.