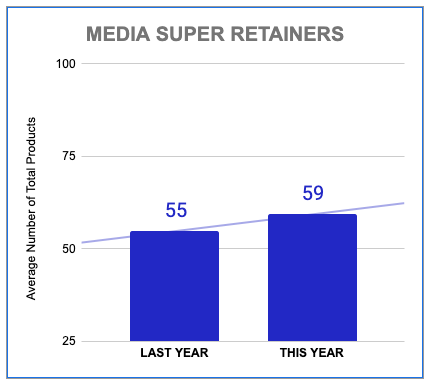

Media Super Retainers tend to have smaller product catalogs. In the last 12 months they had an average of 59 products in their catalog. All other Media Customers had an average of 83 products.

A product in this case is a distinct offering listed under its own “SKU” in the catalog, compared to a rate plan, which is a pricing model to sell that SKU. For example, if The New York Times offers Wordle access on both a monthly and annual payment plan then we would consider that one product/SKU with two rate plans.

Now back to the observation, this could suggest Super Retainers have better control over their business model. Requiring fewer distinct offerings to drive the results that have made them Super Retainers in the first place.

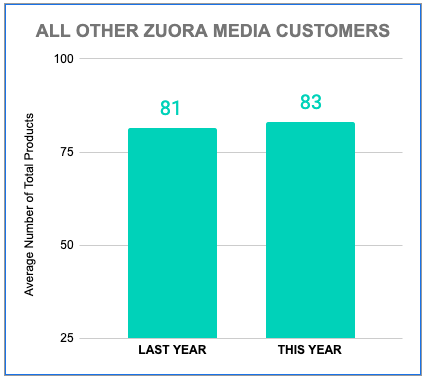

At the same time, the pace of innovation of Super Retainers in the media space is impressive. Not only did they launch more products in total, those new products represented a larger rate of growth of their offerings. Super Retainers grew their offering size by 7% (from 55 products to 59) vs. only 2% (from 81 products to 83) for all other media customers.

Figures 1&2: Average Total Active Products for a Customer in the Cohort

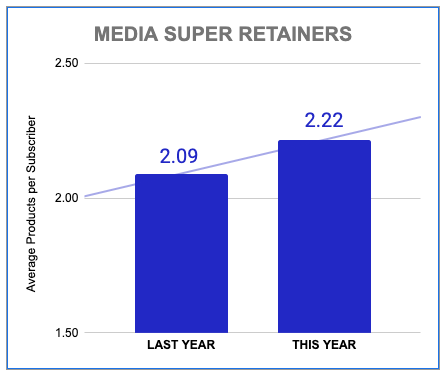

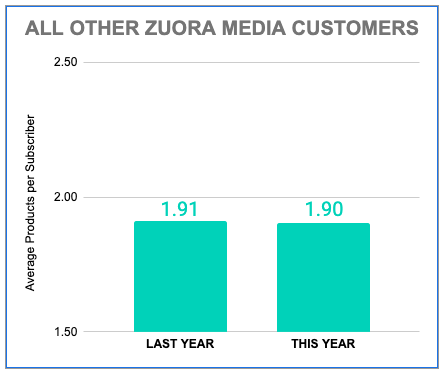

Not only are Media Super Retainers launching more products overall, they’re finding ways to grow the number of products per subscriber. On average, media Super Retainers went from 2.09 to 2.22 products per subscriber from last year to this year. Everybody else in the Media industry stayed basically flat at 1.9.

Given Super Retainers, by definition, have great ARPA growth, this finding would suggest that ARPA growth is being driven by selling net new offerings to customers, not selling more of existing offerings.

Figures 3&4: Average Products per Subscriber

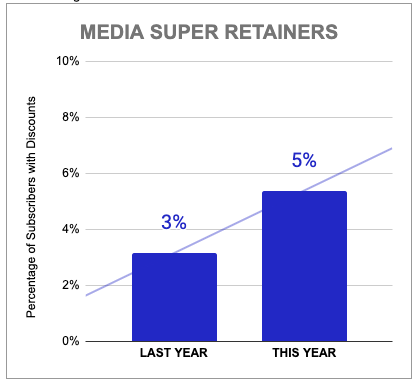

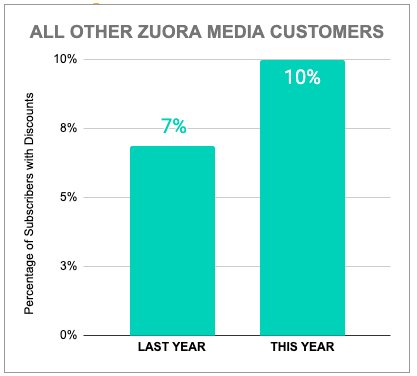

This finding was the most striking due to the large difference between super retainers and all others in the Media cohort. In the last 12 months, the typical Media Super Retainer only gave 5% of their active subscribers a discount. That same metric was 10% for all other Media customers. Effectively Super Retainers discounted half as much as all other peers in their space. What’s also notable is a secular increase in discounting across the entire industry.

Figures 5&6: Average Products per Subscriber