Revenue recognition is complex.

We make it simple.

Reduce risk and lower accounting costs with a fully automated revenue recognition solution that handles any combination of subscriptions, one-time charges, and usage-based offers. Automate all five steps of ASC 606 and IFRS 15, deliver audit-ready revenue, and cut month-end close times by up to 50% with Zuora Revenue — the #1 revenue recognition solution built for finance teams.

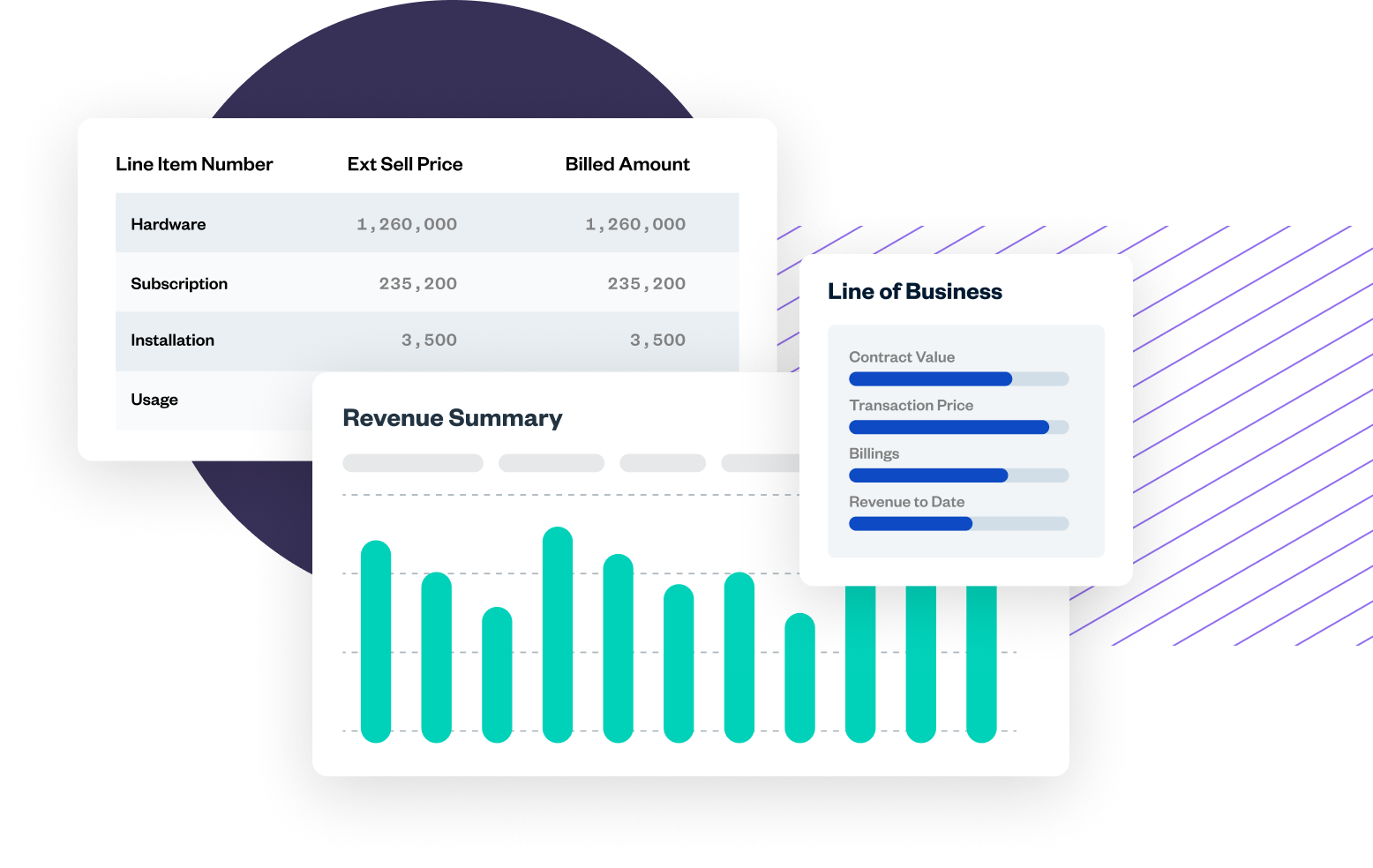

Streamline SSP Analysis: Analyze historical transaction data, calculate standalone selling prices, and automatically allocate transaction values across complex deals.

Meet Compliance: Automate all 5 ASC 606 steps, align with IFRS 15, and generate disclosure-ready reports out of the box.

Effortlessly Go Live on Zuora Revenue

With pre-built connectors to leading ERPs, compatibility to Amazon Web Services & Microsoft Azure, and a one-click onboarding experience, Zuora Revenue easily fits into any ecosystem. You can expect to get started quick and see value fast.

Stacked with value

Greater value, less code with Zuora’s new SDK and APIs.

Achieve real-time visibility into every stage of your revenue lifecycle. With Zuora Revenue, finance teams can reconcile data continuously, identify variances instantly, and close the books up to 50% faster.

Close process dashboard:

Validate revenue data, detect anomalies, and resolve exceptions using the Close Process Dashboard for instant accuracy across reporting periods.

Revenue trend analysis:

Visualize period-over-period revenue changes, uncover causes of fluctuations, and make proactive adjustments before close.

Revenue Analysis:

Compare planned vs. actual revenue, resolve discrepancies, and track recognition progress through real-time analytics.

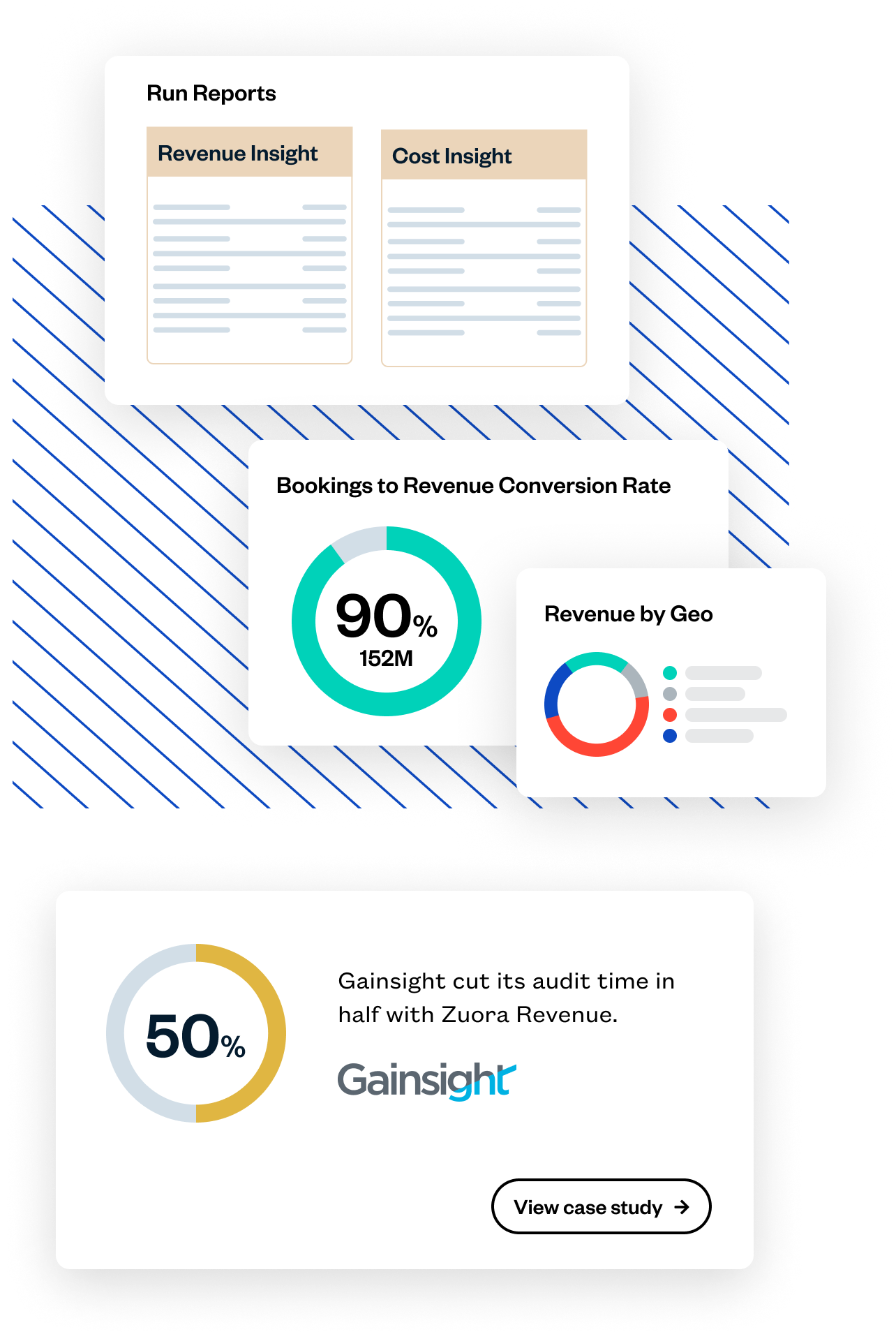

Riverbed reduced its SSP analysis time by over 90% with Zuora Revenue.

Eliminate manual reporting and gain instant insight with Zuora Revenue’s 60+ pre-built reports and real-time dashboards.

Out-of-the-box analytics: Access pre-configured reports for revenue waterfalls, disclosures, VC insights, SOX, and more.

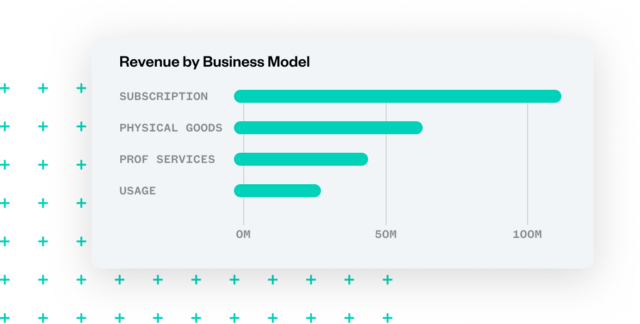

Real-time revenue visibility: View recognized revenue by product, model, and region from a single dashboard.

Connected bookings-to-revenue data: Use live conversion data to predict performance and accelerate decision-making.

Monetize new revenue streams without prolonging your close

Adapt to evolving pricing strategies — from trials and bundles to performance-based contracts — while closing the books on time. Zuora Revenue automates recognition for every monetization model, ensuring compliance and agility.

Seamlessly launch discounts, free trials and bundles

Immediately recognize revenue from any combination of products, services, and subscriptions. Configure revenue recognition rules for any pricing model, allowing rev rec to take place as soon as data comes in.

Recognize delivery-based revenue in real time

Automate delivery-based revenue recognition and manage contract changes mid-cycle — without disrupting downstream billing or financial reporting.

Automatically identify performance obligations

Continuously drive recurring revenue and maximize cross-sell and up-sell opportunities with visibility into the entire customer lifecycle.

Accelerate SSP allocation

Automate standalone selling price (SSP) calculation and allocation for faster, more accurate compliance with ASC 606 and IFRS 15.

One part of the leading Order-to-Cash suite.

Zuora Revenue integrates seamlessly with Zuora Billing, Zuora Collections, and Zuora CPQ to deliver a unified Order-to-Cash experience.

Gain complete visibility across Bookings, Billing, and Revenue — empowering finance, sales, and operations to work from one source of truth.

Trusted by enterprises like Zendesk, Box, and Siemens Healthineers, Zuora’s Order-to-Cash suite ensures every transaction stays compliant, auditable, and optimized for growth

Before Zuora, our finance teams were constantly buried in manual tasks: managing complex contracts, reconciling disparate data, correcting billing errors. The automation Zuora brought has liberated them to focus on strategic analysis and optimization. We’ve seen our automated workflow tasks double.”

— Sid Sanghvi, Head of Finance Business Applications, Asana

“We did the manual revenue for two months — and that was two months too long. Having automation in place means I can spend time analyzing, improving, and building. My team’s work is more strategic now — we’re not just processing transactions.”

"Zuora Revenue was designed from the ground up around the needs of revenue accountants. After just one quarter, our team experienced numerous benefits. The bundle configuration improved the accuracy of our revenue allocations, the customizable grouping rule setup eliminated tedious manual tasks for close, and the user-friendly interface extended us increased functionality and convenience.”

"We have already benefited from significant time savings and cost savings with Zuora Revenue. From contract modifications being calculated automatically to mass updates on data using the solution’s user-friendly interface, Zuora Revenue has been a game-changer for our organization.”

Automated Revenue Management Market Ratings and Buyer’s Guide by MGI Research

In this MGI 360 Market Ratings Report (MRR) and Buyer’s Guide, you’ll learn how Zuora Revenue’s differentiated capabilities stood out to become recognized as the #1 Product for Revenue Automation by a considerable margin.

Avoid Surprise AJEs and Expensive Audits with Zuora Revenue

Join this webinar to hear the experts discuss how Zuora Revenue allows businesses to establish a scalable revenue recognition process that can minimize AJEs and audit fees.

Zuora Revenue is an enterprise-grade revenue automation solution that helps finance teams manage complex revenue recognition across subscriptions, usage-based, and hybrid models. It ensures compliance with ASC 606 and IFRS 15 while providing real-time visibility into revenue performance.

How does Zuora Revenue automate revenue recognition?

Zuora Revenue automatically applies configurable recognition rules to transactions based on performance obligations, pricing models, and contract changes. It integrates with ERP, CRM, and billing systems to reconcile data in real time, reducing manual work and accelerating financial close by up to 50%.

Can Zuora Revenue handle ASC 606 and IFRS 15 compliance?

Yes. Zuora Revenue automates all five steps of ASC 606 and IFRS 15 for complex, multi-element contracts. The platform manages SSP allocation, contract modifications, and disclosure reporting — ensuring complete compliance and audit readiness.

How does Zuora Revenue integrate with ERP and billing systems?

Zuora Revenue offers pre-built connectors and open APIs for seamless integration with systems such as Salesforce, SAP, Oracle NetSuite, and Workday. This enables synchronized data flow across billing, bookings, and revenue — creating a unified, end-to-end Order-to-Cash process.

What results have customers achieved with Zuora Revenue?

Enterprise customers such as Gainsight, AppDynamics, and Riverbed have reported measurable improvements, including:

90% faster SSP analysis

40% shorter financial close cycles

50% reduced audit preparation time

These outcomes demonstrate the platform’s ability to deliver speed, accuracy, and compliance at scale.

How does Zuora Revenue support continuous accounting?

Zuora Revenue enables continuous accounting by reconciling data automatically throughout each period. Finance teams can identify anomalies in real time, run automated trial balances, and ensure accurate revenue reporting without waiting for month-end close.

What types of revenue models does Zuora revenue recognition software support?

Zuora revenue recognition software supports several revenue models such as subscriptions, usage-based, hybrid, milestones, and services — all automated for recognition and forecasting.

How does Zuora revenue recognition software accelerate the close process?

Zuora revenue recognition software accelerates the close process by continuous accounting and allowing you to recognize revenue daily, cutting month-end close times by up to 50%.

How does Zuora revenue recognition software ensure audit readiness?

Zuora revenue recognition software ensures audit readiness with SOX/SOC controls, role-based security, and a complete audit trail of every recognition entry.

How is Zuora Revenue different from other revenue recognition software?

Unlike traditional ERP modules, Zuora Revenue is built for modern monetization models — subscriptions, usage, hybrid, and one-time sales. It combines automation, compliance, and analytics in a single system, reducing complexity and accelerating growth across business models.

Your journey starts here

As your customers change how they want to access your products and services, you have to evolve how you do business. Learn more about how our leading Subscription Economy® solutions have helped many of the world’s most innovative subscription businesses succeed.