Smart Collections: Payment Reminder Strategies That Actually Work in Recurring Revenue

How you collect has a direct impact on your customer relationships and, in the end, what you collect.

Smart collections is a segmented, AI-assisted approach to payment reminders and collections that adapts outreach by account value, payment behavior, risk, and customer context. In recurring revenue, the goal is to recover cash while protecting the customer relationship, using automation for routine follow-up and human escalation where it matters most.

For decades, collections has lived at the bottom of the AR org chart. It was the place where overdue invoices went to be chased, where the team’s only KPI was dollars collected this month, and where the playbook was variations on the same theme: send a reminder, send a firmer reminder, send a final notice, escalate. The implicit assumption was that the customer relationship had already done its work by the time the invoice was overdue, and collections was just the cleanup function.

That assumption made sense in a one-time-transaction business. Sell the product, ship it, invoice for it, get paid. If the customer never came back, that was fine. The cleanup function could afford to be aggressive because the relationship was already complete.

In recurring revenue, none of that is true. Every overdue customer today is a customer who is supposed to renew next quarter. Every dunning interaction is a customer experience moment that either builds trust or erodes it. Aggressive collections on a strategic account because of a $500 administrative dispute can cost a $5M renewal. Underdunning a long-tail account because the team is too cautious can leave six figures of recoverable cash on the table. The same playbook doesn’t work for both customers, and the cost of using one playbook is paid in churn.

Smart collections is the operating model that fixes this. It segments customers by value and payment behavior. It calibrates tone to the aging stage and the customer context. It orchestrates channels strategically so they reinforce rather than annoy. It uses AI to score accounts, draft outreach, and assist with reply classification and routing. The job becomes pattern recognition rather than blanket pressure, and when designed well, the result can be stronger cash recovery with less damage to customer trust.

Why Traditional Collections Fail in Recurring Revenue

Traditional collections were designed for a different business model. The invoice represented the end of the customer relationship, not a checkpoint in the middle. The collections team’s job was to recover cash on a transaction the customer was unlikely to repeat. Aggressive tactics were rational because the cost of damaging the relationship was zero.

In recurring revenue, the cost of damaging the relationship is the entire LTV of the account. That changes the math, and it should change the playbook.

The One-Time-Transaction Mindset

If you measure your collections team only on dollars collected this month, you implicitly tell them to use whatever tactics work to collect this month’s dollars. Service shutoffs, threatening language, blanket dunning regardless of context, and escalations that loop in legal before the account team has been informed. These tactics can produce a strong month-over-month collections number. They also produce churn six months later that wipes out the gains, and then some.

The tactics aren’t the problem. The KPI is the problem. Modern collections teams need to be measured on cash collected, customer retention impact, and dispute resolution speed simultaneously, which is the multi-metric framing modern smart collections programs are built around.

The Cost of Aggressive Dunning in Recurring Revenue

Consider a hypothetical example that recurring-revenue AR leaders see variations of regularly. A customer has a $5M ARR contract. The AR team sends a $500 invoice that bounces because of an expired card. The automated dunning workflow fires. Day 1, friendly reminder. Day 7, firmer reminder. Day 14, escalation-tone reminder, copying the customer’s CFO. Day 21, service-throttling notice.

The customer’s AP team eventually notices the bounce and updates the card. The $500 lands. The collections team marks the account as resolved.

Six months later, the account doesn’t renew. The customer’s CFO remembers being copied on what felt like a threat over a $500 administrative issue. The CSM team didn’t know it was happening because collections operates outside their tooling. The account management lead found out in the renewal conversation.

The resulting calculations are brutal. You collected $500 collected but lost $5M. The dunning workflow did exactly what it was designed to do; it’s just that the design was wrong for the business model.

The Cost of Underdunning Strategic Accounts

The opposite failure mode is just as expensive, and it’s more common than most teams realize. The collections team is afraid to push on a strategic account, so the account stays in the 60-90 day aging bucket for a quarter. The customer eventually pays, but the cash arrived three months late, the AR aging report looks worse than the customer’s actual creditworthiness justifies, and the FP&A team has been forecasting cash inflows that never materialize on time.

In a recurring-revenue business, the answer isn’t to dun harder. It’s to involve the right humans (account team, customer success, sometimes the customer’s CFO) earlier and through the right channels.

The Pattern Mismatch

Blanket cadences fail because customer payment behavior in recurring revenue varies enormously by ARR tier, region, industry, payment-method coverage, and lifecycle stage. A strategic SaaS customer in the EU on annual invoicing has nothing in common, behaviorally, with a long-tail SMB customer in the US on monthly card billing. Putting them into the same workflow is operationally simpler, but the cost shows up in the retention and recovery numbers later.

The Principles of Smart Collections

Smart collections is segmented, automated, AI-augmented payment-reminder workflows that adapt to each customer’s value, risk profile, payment behavior, and channel preference. It replaces blanket dunning with contextual outreach designed to preserve the customer relationship while recovering cash.

The principles below are what distinguish a smart collections program from a traditional one. None of them is individually novel; the combination is what produces results.

Segmentation by Customer Value and Payment Behavior

The starting point. Every collections workflow should be defined for a specific segment, not a global default. Useful segmentation dimensions include:

- ARR tier. Strategic accounts, mid-market, long-tail. Each gets a different cadence, channel mix, and escalation path.

- Payment-behavior cohort. Customers who consistently pay on time, customers who reliably pay 5-10 days late, customers with sporadic late payments, and customers with chronic delinquency.

- Risk score. Externally sourced (Dun & Bradstreet, Experian) or internally derived (payment history, churn-risk signals).

- Strategic relationship value. Logo accounts, accounts with expansion potential, accounts that the broader business has reasons to protect.

Segmentation rules should be configurable by Finance and RevOps, not hard-coded by IT. The segmentation model evolves as the business learns.

Personalization of Tone, Channel, and Timing

Each segment gets a calibrated journey. Long-tail accounts on monthly card billing might get a fully automated email cadence with a tone that stays warm through Day 14 and only sharpens at Day 30+. Mid-market accounts get a blended journey: automated reminders for the first three touches, manual collector intervention from the second week onward. Strategic accounts get the account team in the loop from Day 1.

Tone is calibrated to the aging stage. Pre-due reminders should sound like a courtesy. Day-1 reminders should sound matter-of-fact. Day-30 reminders should sound serious without sounding adversarial. The right copy gets generated through templates, AI augmentation, and collector review for the highest-value accounts.

Multi-Channel Orchestration

A smart collections strategy may use email, customer-portal or in-app prompts, SMS, and account-team outreach depending on segment, consent, and system setup. Email is usually the default, but it isn’t always the right channel. In-app prompts can surface the reminder where the customer is already engaged with the product. SMS earns higher immediate visibility than email but should be used with consent, segment controls, and frequency caps. Account-team direct outreach is the highest-touch and most expensive option, reserved for accounts that warrant it.

Channels should sequence rather than compete. A typical mid-market post-due cadence might run: Day 1 email, Day 3 in-app prompt, Day 7 email plus SMS, Day 14 collector phone call, Day 30 account-team escalation. Each touch reinforces rather than duplicates the previous one. Confirm which channels are native, configured through workflow, or integrated through third-party systems before publishing channel-specific product claims.

Audit-Grade Workflow Logging

Every touchpoint should be logged with user, timestamp, channel, and outcome. This is the control baseline for any modern collections platform, and it’s what makes the difference between a smart collections program that controllers and auditors can defend and a tactical collections operation built on a customer-success email tool.

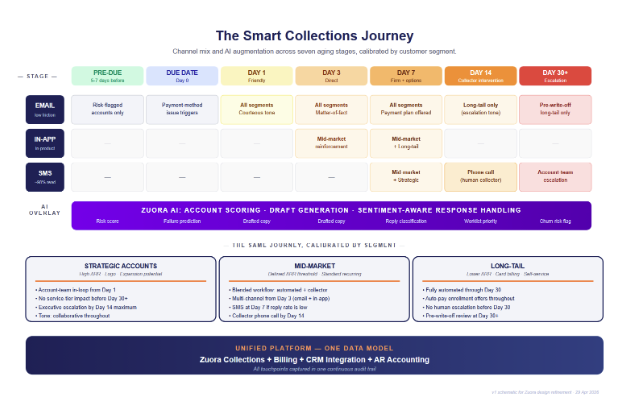

Designing the Smart Collections Journey

The visual below shows the seven-stage cadence that defines a smart collections journey across three channels.

Pre-Due Reminders

Pre-due reminders work for some segments and backfire on others. They work for customers with known payment-method risks (recently expired cards, recent ACH failures), customers with seasonally late patterns, and customers who have explicitly opted in to advance notification. They backfire on customers who consistently pay on time and read pre-due nudges as either annoying or, worse, distrustful.

The rule of thumb is to trigger pre-due reminders based on customer payment-history risk, not as a default for everyone. Five to seven days before the due date is a reasonable window for the segments that benefit from them.

Due-Date Workflows

The due-date touch is most useful for accounts with known issues like payment-method failures, expired stored credentials, and recent dispute history. For most healthy accounts, no due-date touch is required, and the journey starts post-due if the payment doesn’t land.

For accounts that do warrant the touch, the workflow should attempt automated resolution first (retry the payment with the stored method, retry with a backup method if available) before any human-facing reminder.

Post-Due Cadences

The core of the smart collections journey. A typical post-due cadence runs through five stages, with tone calibrated to the segment.

- Day 1. Friendly notification. Tone: courteous, assumes the customer simply forgot or hit a payment-method issue. Channel: email primary, sometimes paired with in-app for mid-market accounts.

- Day 3. Direct reminder. Tone: matter-of-fact, references the specific invoice and an easy resolution path. Channel: email, with in-app reinforcement.

- Day 7. Firm reminder with options. Tone: more direct, mentions the aging, offers a payment plan, or dispute resolution path. Channel: email plus SMS for higher-ARR segments.

- Day 14. Collector intervention for mid-market and strategic accounts. Long-tail accounts get an automated escalation tone reminder. Channel: phone for high-touch segments, escalated email for everyone else.

- Day 30+. Account-team escalation for strategic accounts. Pre-write-off review for long-tail. Service-tier impact decisions for mid-market.

The cadence is segmented, but the structure is consistent across segments. What varies is the tone, the channel mix, and where the human enters the workflow. This is the operational layer that dunning management describes more narrowly; smart collections is the strategic layer that orchestrates dunning and the human work above it.

Combining Email, In-App, and SMS

Channel selection is one of the higher-leverage decisions in a smart collections design. Each channel has different reach, cost, friction, and customer-perception profiles. The mix that works depends on the segment.

Channel Selection by Segment

- Long-tail accounts. Email is usually sufficient. The economics don’t justify SMS or account team involvement, and most long-tail customers prefer to handle billing through email.

- Mid-market accounts. Email plus in-app is the typical mix, with collector phone outreach starting at Day 14 for accounts above a defined ARR threshold.

- Strategic accounts. Account-team outreach should start before any automated message lands. The cadence here is less about reminders and more about coordinated executive-level conversations with finance support.

Sequencing Across Channels

Email opens are weak signals: they tell you the message was delivered and possibly opened, but not that the customer engaged. Customer-portal or in-app interactions can be stronger signals when the customer is already active in the product experience. SMS often earns higher immediate visibility than email, but it should be used carefully, with consent, segment controls, and frequency caps.

The implication: sequence channels from low-friction to higher-friction. Start with email. Add in-app at the second touch. Add SMS at the third touch for higher-value segments. Each escalation should give the customer one more clear pathway to resolution before pressure builds.

Frequency Caps to Prevent Annoyance

Over-touching erodes the relationship even when the intent is good. Many teams set frequency caps, such as one touch per channel per day and a weekly account-level cap. The cap protects accounts that are already paying attention from feeling pressured, and it forces the workflow design to be efficient rather than relying on volume to land the message.

Escalations Without Burning the Relationship

Escalation is where smart collections programs most often distinguish themselves from tactical dunning operations. The decision whether to escalate, who to escalate to, and how to escalate determines whether the workflow recovers cash or burns the relationship.

When to Escalate from Email to a Human

Escalation should be triggered by thresholds, not by collector judgment alone. Predictable thresholds remove emotion from the decision. Useful triggers include:

- Aging beyond a defined window (commonly 14 or 21 days post-due, depending on segment).

- ARR above a threshold, combined with no customer-success signal explaining the delay.

- A pattern of repeated short pays without remittance advice.

- Customer replies that indicate dispute, dissatisfaction, or relationship risk.

The thresholds should be tunable by segment, and they should be reviewable by the controller, so escalation rules are part of the audit trail rather than tribal knowledge.

How Account Teams Should Step In

Sales, customer success, and account management each have a role in escalations, and the role differs by segment. For strategic accounts, the account management lead is usually the right contact for any escalation past Day 14. For mid-market, customer success often plays this role. For long-tail accounts, escalation is rarely worth the human cost; instead, the workflow should drive to write-off or service-tier impact decisions.

The handoff from automation to a human should preserve context. The collector or account team owner should see the full history of touchpoints, customer replies, dispute markers, and any related CRM signals before they engage. CRM integration is what makes this work; without it, the human re-enters the conversation cold, and the relationship-preservation argument falls apart.

Service-Tier Impact Decisions

Throttling service, suspending access, or restricting features are real tools, but they should sit at the end of the escalation path, not the middle. Service impact is the highest-friction lever a collections team can pull, and it should be reserved for accounts where the cash-recovery probability is high and the relationship-preservation cost is low (typically chronic delinquents on long-tail tier, or accounts that have explicitly indicated they’re churning).

For strategic and mid-market accounts, service impact should be the absolute last step before write-off. Any earlier deployment risks turning a recoverable relationship into a churn certainty.

AI in Smart Collections

The principles discussed here describe a workflow that’s complex enough to fail without help. AI is what makes smart collections operationally feasible at scale. It augments the collector rather than replacing them, and it focuses on the parts of the workflow that humans do least well: ranking large worklists, drafting consistent copy, and classifying inbound replies.

Account Scoring and Prioritization

A collections team has a finite number of human hours. The question is which accounts get those hours. AI account scoring ranks the worklist by which interventions will actually move the needle, based on payment-history patterns, ARR, dispute markers, customer-success signals, and historical recovery rates. The collector starts the day on the accounts most likely to benefit from human attention, and the rest of the workflow runs on automation.

AI-Drafted Outreach (Review-and-Send)

Writing payment reminders is repetitive work that humans do inconsistently. AI generates the first version of every reminder, sized to the customer’s history and tone, with the specific invoice context embedded. The collector confirms or edits before sending for high-value accounts, or lets the workflow auto-send for lower-tier segments. Consistent tone calibration becomes a workflow property rather than a collector skill.

AI-Assisted Response Handling

Customer replies to payment reminders fall into a few patterns: routine acknowledgment, payment promise, dispute indication, and frustration. A well-designed smart collections workflow handles each pattern differently. Routine acknowledgments move toward automatic closeout. Disputes route to a human with the full context. Frustration signals reach the account team for an early-warning touch. AI can assist with classifying inbound replies so the workflow routes them quickly.

The capabilities running underneath this are part of Zuora AI, and the AI for Collectors program describes the operational integration into the collections workflow. For finance teams thinking about the next phase (fully autonomous AR agents), the AI agents for accounts receivable deep dive covers the strategic frame.

Measuring Smart Collections Effectiveness

The metrics matter because they shape the team’s behavior. A team measured only on cash collected this month will revert to blanket dunning. A team measured on a balanced scorecard will build smart collections.

Collection Rate

The headline metric. Percentage of overdue invoices recovered without escalation past a defined threshold (often Day 30). High-performing smart collections programs aim to recover a meaningful share of overdue cash in the first three touches, before escalation costs rise.

Customer Response Rate

Reply rate by channel and by segment. A drop in response rate is a leading indicator that the workflow is being ignored or that customers have learned to filter the messaging. Reply classification and collector review can help distinguish routine delays from disputes or relationship risk.

Churn Impact

The metric most teams don’t measure and the one that matters most in recurring revenue. How often is churn attributable to the collections experience? Tracking this requires CRM integration and a willingness to look critically at the workflow when the answer is uncomfortable. Teams that measure this consistently end up redesigning their cadences, not just iterating on copy.

Recovery Without Escalation

The operational health metric. The percentage of overdue cash recovered in the first three touches, before any human collector intervention. A high percentage means the automation is doing its job. A low percentage means too many accounts need escalation, which usually points to underlying segmentation or workflow design issues.

How Zuora Powers Smart Collections

The architectural commitment matters. Zuora delivers smart collections as a configurable workflow inside Zuora Collections, running on the same data model as the billing system of record. The structural advantages are current invoice context, the Salesforce sync and broader CRM/support-system integrations, and a connected audit trail across collections, cash application, and AR accounting.

Zuora Collections Workflow Engine

Cadences, segmentation rules, escalation thresholds, channel logic, and frequency caps should be configurable by Finance and RevOps with minimal engineering involvement, so teams can iterate faster than a traditional software-release cycle. The team can refine the workflow as it learns, rather than queuing changes against an IT roadmap.

AI Capabilities Out of the Box

Zuora Collections uses AI-generated insights and health scores to help teams segment and prioritize accounts based on payment behavior, engagement patterns, and risk indicators. It also supports contextual collections workflows, collector dashboards, task management, forecasting, and CRM/communication-platform integrations, so teams can coordinate outreach with more context. The AI runs on the same data model as the collections workflow, which is what makes its outputs trustworthy: clean billing data goes in, contextual outreach comes out.

CRM Integration

The Salesforce sync, along with broader CRM and support-system integrations, helps collections teams see account context before escalating.

One Continuous Audit Trail

Every touchpoint, every reply, every escalation decision is logged with user, timestamp, channel, and outcome. The trail is queryable by the controller, reviewable in a customer dispute, and defensible to an external auditor. It is also the input data for the next iteration of the workflow design, because measuring what’s working requires the data to be there in the first place.

Collect Cash and Keep Customers

Smart collections is the operating model that lets a recurring-revenue business do both. The work is segmentation, channel orchestration, AI-augmented intelligence, and audit-grade logging. The platform requirement is a connected AR architecture where collections, billing, and CRM share a data model, so the journey can be contextual and the audit trail can be continuous.

When designed well, smart collections can help teams recover cash while protecting customer relationships. The goal is not to make collections softer or harsher; it is to make collections more contextual, more coordinated, and easier to audit.

Ready to design a smart collections program?

FAQs

1.

What software supports smart collections and payment reminders?

Smart collections software should support configurable workflows, segmented cadences, collector dashboards, task management, account prioritization, customer-context integration, audit trails, and reporting. Zuora Collections supports contextual collections workflows, collector dashboards, task management, forecasting, and CRM/communication-platform integrations.

2.

What are smart collections?

Smart collections is a segmented, AI-assisted approach to payment reminders and collections that adapts outreach by account value, payment behavior, risk, and customer context. It replaces blanket dunning with contextual outreach designed to preserve the customer relationship while recovering cash. A smart collections strategy may use email, customer-portal or in-app prompts, SMS, and account-team outreach depending on segment, consent, and system setup.

3.

How does AI help with payment reminders?

AI can help with payment reminders by ranking which accounts need human attention first and by drafting consistent, context-aware copy at scale. Source-safe capabilities include AI-generated insights, health scores, forecasting, prioritization, and AI-assisted reply classification/routing for faster follow-up.

4.

How do you write a payment reminder that doesn't lose the customer?

A relationship-preserving payment reminder follows four rules. It is contextual, referencing the specific invoice, contract, and customer history rather than a generic template. It is calibrated to the aging stage: warmer tone for pre-due, more direct for post-due, escalation-ready for 30+ days. It offers a clear and easy resolution path, such as a one-click payment link or a direct line to a human contact. And it acknowledges the relationship, with no threats or service-shutoff implications until escalation has been reached. AI-drafted copy can produce these characteristics consistently at scale, with collector review for high-value accounts.

5.

What is the difference between dunning and collections?

Dunning is the specific automated process of sending payment reminders for overdue invoices on a defined cadence. It is one tactical workflow within the broader collections function. Collections is the strategic function responsible for recovering all overdue receivables, including dunning workflows, dispute resolution, account-team escalations, payment plan negotiations, and write-off decisions. In modern smart collections programs, dunning is the automated bottom layer, AI augments the middle (account scoring and draft outreach), and human collectors handle the high-value top layer.

6.

How do automated payment reminders work?

Automated payment reminders work by triggering a configurable workflow when an invoice reaches a defined aging stage. The workflow applies segmentation rules to determine tone, timing, frequency, and configured channels; logs the activity; and routes follow-up based on the customer response. Smart implementations can layer in AI-generated insights, health scores, prioritization, AI-assisted reply classification/routing, and CRM context so the broader account team has visibility into collections activity.

7.

How do you escalate collections without damaging the customer relationship?

Escalating collections without burning the relationship requires three things. First, threshold-based triggers, so escalation happens predictably rather than emotionally (for example, 30 days post-due plus a defined ARR threshold plus no customer-success signal that explains the delay). Second, the right escalation owner: the account-team contact for strategic accounts, a collections lead for mid-market, and automated workflows for long-tail. Third, escalation messaging that acknowledges the relationship and offers options (payment plan, dispute resolution, account-team conversation) rather than only threats. Service-tier impact decisions should sit at the end of the escalation path, not the middle.

8.

What features should I look for in collections software?

Enterprise-grade smart collections software should support configurable workflows, segmented cadences, collector dashboards, task management, account prioritization, customer-context integration, audit trails, and reporting. If using AI claims, specify supported capabilities such as health scores, forecasting, prioritization, and AI-assisted outreach rather than implying autonomous handling unless Product confirms. When evaluating, ask whether the software operates on current invoice, payment, customer, and collections data, or whether teams must reconcile context across exports and disconnected systems.