Ohio Representative Michael G. Oxley was a straight-arrow former FBI agent who was serving as chairman of the House Financial Services Committee when the Enron and WorldCom dominoes began to fall. Before he came to Congress, he knew little to nothing about corporate finance. He was much more experienced with stolen cars, kidnappings, and bank robberies.

As he told the Securities and Exchange Commission Historical Society in 2012:

“I graduated from law school at Ohio State in ’69, and then I was recruited by the FBI and I went in the Bureau. Though I did have some experience – I was on the bank robbery squad, so I investigated unauthorized withdrawals from banking institutions. That was quite interesting. Then when I retired from the Bureau, I went back to my hometown of Findlay, Ohio, and joined my dad’s law practice. But I never had that much experience in the overall financial world until I came to Congress.”

But by the time of the Enron scandal, Oxley had 20 years of congressional experience investigating corporate monopolies (the break-up of AT&T and Ma Bell), prosecuting insider trading (Michael Milken), managing the savings and loan crisis, and modernizing the finance industry. Oxley was also the man responsible for introducing Wall Street to decimals – stocks used to be traded in eighths because the coin of the realm at the market’s founding in 1792 was the Spanish doubloon (!).

In 2002, however, Oxley faced a problem of an entirely different magnitude. If you missed Part 1 of our story, here’s the TL;DR: The Enron crisis was not just the implosion of some local Ponzi scheme, it exposed a rot that could mean the collapse of the country’s entire financial system. Enron, Tyco, Worldcom showed that companies were falsifying their financial statements, and the auditors who were supposed to be guarding against this, including Arthur Andersen, the biggest and oldest auditing firm, were co-conspirators in the fraud. If you could not trust a company’s financial statements, then how could you ever invest in them with confidence?

The whole system had one foot in the grave, and the other on a banana peel. People were demanding a legislative response, and Oxley threw himself at the problem. Here’s what he said in a 2004 interview:

“We scheduled 10 hearings over a six-week period, during which we brought in some of the best people in the country to testify … The hearings produced remarkable consensus on the nature of the problems: inadequate oversight of accountants, lack of auditor independence, weak corporate governance procedures, stock analysts’ conflict of interests, inadequate disclosure provisions, and grossly inadequate funding of the Securities and Exchange Commission.”

After a heroic legislative effort, Oxley’s bill in the House was eventually combined with Maryland Senator Paul Sarbane’s bill in the Senate to become the Sarbanes-Oxley Act, commonly referred to as SOX. Only three people in the Senate and the House voted against it. On July 30, 2002, President George W. Bush signed it into law, stating it included “the most far-reaching reforms of American business practices since the time of Franklin D. Roosevelt.”

SOX had four key goals: To enhance transparency through reliable financial statements, increase corporate accountability by holding executives responsible for their reports, prevent fraud through stricter internal controls, and restore investor confidence.

How did it aim to achieve those goals?

First, by forcing companies to implement strong financial controls that prevent fraud from occurring. The famous “Section 404” of the bill not only mandated new internal rules and checks to prevent fraud, but also told management teams to report on the effectiveness of those controls.

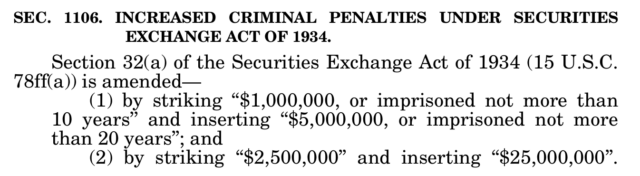

Second, by making executives put their careers — and their literal freedom — on the line. Not only did the bill make CEOs and CFOS personally certify the accuracy of their financial reports, but it also significantly increased their potential criminal penalties (even if they didn’t directly commit the fraud):

And finally, by creating the Public Company Accounting Oversight Board, a new government agency intended to audit the auditors. The PCAOB set auditing standards, inspected audit firms, and generally enforced the rules.

As Oxley noted: “Heretofore, the accounting industry had been self-policed. The abject failure of Arthur Andersen in those circumstances called for a paradigm change. I think there was virtually no opposition to creation of the PCAOB.”

Who would watch the watchmen? The PCAOB.

At last, the American economy had real regulatory oversight and legal accountability. As PCAOB Member Steven B. Harris said, “It restored investor confidence.”

SOX reshaped American business forever — but who do we have to thank for bringing this sweeping legislation to life? In the next and final installment, we’ll meet some of the renegade accountants who helped save the system from total collapse.