string(5) "false"

array(33) {

["thank_title"]=>

string(0) ""

["thank_subtitle"]=>

string(0) ""

["ty_asset_cta_text"]=>

string(0) ""

["_id"]=>

string(7) "1ca23f8"

["__dynamic__"]=>

array(10) {

["marketo_form_id"]=>

string(126) "[elementor-tag id="400f210" name="acf-text" settings="%7B%22key%22%3A%22field_584ecc5e4e534%3Aresource_marketo_form_id%22%7D"]"

["cid"]=>

string(117) "[elementor-tag id="d9e3696" name="acf-text" settings="%7B%22key%22%3A%22field_5914cef4114b8%3Acampaign_id_cid%22%7D"]"

["form_title"]=>

string(120) "[elementor-tag id="94692c4" name="acf-text" settings="%7B%22key%22%3A%22field_584ecc644e535%3Amarketo_form_title%22%7D"]"

["form_sub_title"]=>

string(124) "[elementor-tag id="6de01ff" name="acf-text" settings="%7B%22key%22%3A%22field_584ecc6d4e536%3Amarketo_form_sub_title%22%7D"]"

["ty_title"]=>

string(110) "[elementor-tag id="24b925b" name="acf-text" settings="%7B%22key%22%3A%22field_584ecc804e537%3Aty_title%22%7D"]"

["ty_subtitle"]=>

string(113) "[elementor-tag id="e3ede35" name="acf-text" settings="%7B%22key%22%3A%22field_584ecc984e538%3Aty_subtitle%22%7D"]"

["ty_description"]=>

string(116) "[elementor-tag id="4e6e511" name="acf-text" settings="%7B%22key%22%3A%22field_588a436376755%3Aty_description%22%7D"]"

["ty_asset_cta"]=>

string(119) "[elementor-tag id="096e012" name="acf-text" settings="%7B%22key%22%3A%22field_588bb1773e106%3Aty_asset_cta_text%22%7D"]"

["ty_url"]=>

string(102) "[elementor-tag id="b25f4c7" name="post-custom-field" settings="%7B%22custom_key%22%3A%22ty_url%22%7D"]"

["ty_asset"]=>

string(104) "[elementor-tag id="8e277e6" name="post-custom-field" settings="%7B%22custom_key%22%3A%22ty_asset%22%7D"]"

}

["language"]=>

string(7) "english"

["marketo_form_id"]=>

string(4) "2180"

["cid"]=>

string(66) "FY19Q3-WEBSTE-GLOBL-VDEO-What's Now and Next in Revenue Operations"

["is_multistep"]=>

string(0) ""

["exclude_personal"]=>

string(0) ""

["vidyard_video_id"]=>

string(0) ""

["form_title"]=>

string(12) "Register Now"

["form_sub_title"]=>

string(0) ""

["ty_title"]=>

string(25) "Thank You For Registering"

["ty_subtitle"]=>

string(27) "We hope you enjoy the video"

["ty_description"]=>

string(202) "

"

["ty_asset"]=>

string(0) ""

["ty_asset_cta"]=>

string(0) ""

["ty_url"]=>

string(0) ""

["content_type"]=>

int(7732)

["template"]=>

string(8) "resource"

["resource_headline"]=>

string(58) "RevPro Keynote - What's Now and Next in Revenue Operations"

["body_copy"]=>

string(355) "Whether you’re new to revenue automation or a seasoned RevPro user, join us for this keynote address where you’ll hear about current challenges for revenue leaders, what’s on the horizon for solving the biggest pains in accounting and revenue recognition, and how technology has evolved help to modernize your revenue operations.

"

["cta_text"]=>

string(9) "watch now"

["form"]=>

bool(true)

["resource_marketo_form_id"]=>

string(4) "2180"

["marketo_form_title"]=>

string(12) "Register Now"

["campaign_id_cid"]=>

string(66) "FY19Q3-WEBSTE-GLOBL-VDEO-What's Now and Next in Revenue Operations"

["timezone"]=>

string(19) "America/Los_Angeles"

["speakers"]=>

array(1) {

[0]=>

object(WP_Post)#10894 (24) {

["ID"]=>

int(36139)

["post_author"]=>

string(3) "115"

["post_date"]=>

string(19) "2017-05-07 20:25:11"

["post_date_gmt"]=>

string(19) "2017-05-08 03:25:11"

["post_content"]=>

string(0) ""

["post_title"]=>

string(11) "Monika Saha"

["post_excerpt"]=>

string(0) ""

["post_status"]=>

string(7) "publish"

["comment_status"]=>

string(4) "open"

["ping_status"]=>

string(6) "closed"

["post_password"]=>

string(0) ""

["post_name"]=>

string(11) "monika-saha"

["to_ping"]=>

string(0) ""

["pinged"]=>

string(0) ""

["post_modified"]=>

string(19) "2017-05-16 17:30:16"

["post_modified_gmt"]=>

string(19) "2017-05-17 00:30:16"

["post_content_filtered"]=>

string(0) ""

["post_parent"]=>

int(0)

["guid"]=>

string(55) "https://zuorainternprd.wpengine.com/people/monika-saha/"

["menu_order"]=>

int(0)

["post_type"]=>

string(6) "person"

["post_mime_type"]=>

string(0) ""

["comment_count"]=>

string(1) "0"

["filter"]=>

string(3) "raw"

}

}

["resouce_selection_type"]=>

string(11) "hand_select"

["selectable_resources"]=>

array(3) {

[0]=>

object(WP_Post)#10998 (24) {

["ID"]=>

int(41598)

["post_author"]=>

string(2) "64"

["post_date"]=>

string(19) "2017-03-30 19:40:47"

["post_date_gmt"]=>

string(19) "2017-03-31 02:40:47"

["post_content"]=>

string(7029) "This post is guest-authored by two experts at Zuora: Peush Patel, Director of Finance and JingJing Xia, Sr. Product Marketing Manager. Zuora is the industry leader in subscription billing, e-commerce and finance and a valued partner of Leeyo Software.

Patel is the Product Management Director for Finance at Zuora. Before Zuora, he led the Revenue Management product at Oracle. He has participated on a recent webinar with Leeyo about RevRec for subscription companies. Xia leads the Product Marketing team at Zuora and leads marketing for the pricing, billing, and finance product areas.

New Revenue Reporting Standards: A Guide for Subscription Companies

The upcoming changes to revenue reporting standards are more than just a headache for your finance department. They can potentially impact the growth engines at the heart of any business—and subscription-based companies are particularly vulnerable to these consequences.

The impact on subscription companies is unique and different. How you prepare for it comes down to how you structure your subscription offerings, the type of contracts you plan to sell, and how you want to recognize revenue.

What’s changing and why?

In 2014, the Federal Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB) issued new standards for recognizing revenue from contracts with customers. The result of a years-long effort, these guidelines will be instituted in 2018 for public companies and 2019 for private firms.

The goal was to simplify and harmonize revenue recognition practices. Currently, requirements for reporting revenue—a critical metric for evaluating a company’s financial performance—vary across different industries, jurisdictions and markets. These discrepancies create incongruent accounting results for economically similar transactions, rendering macro-level comparisons nearly impossible.

The new standards are based on one overarching principle: Companies must recognize revenue when goods and services are transferred to the customer, in an amount that is proportionate to what has been delivered at that point.

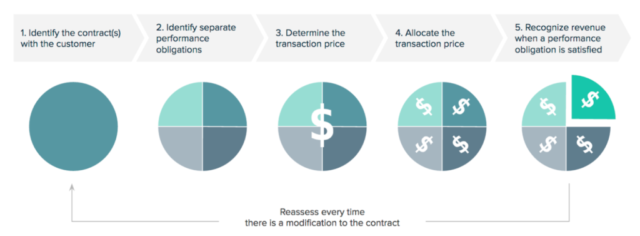

The five-step model

A five-step model summarizes the process for recognizing revenue from contracts with customers:

- Identify the contract with the customer

- Identify the separate performance obligations

- Determine transaction price

- Allocate transaction price

- Recognize revenue when (or as) a performance obligation is satisfied

How will it impact subscription-based companies?

Compliance with the new standards presents a particularly difficult challenge for subscription-based companies, who can be tripped up at each step of the model.

Here’s where the trouble arises:

How will it impact subscription-based companies?

Compliance with the new standards presents a particularly difficult challenge for subscription-based companies, who can be tripped up at each step of the model.

Here’s where the trouble arises:

- Subscriptions change frequently. Whether a customer upgrades, downgrades or adds a few seats, contract changes are the norm. In our experience, every subscription contract undergoes an average of four mid-term changes. These changes can make compliance with step 1 (identify the contract) difficult. In some circumstances, contract changes are handled as a modification to the existing contract, while in other situations, a separate contract is created. Revenue recognition is impacted accordingly.

- Subscriptions are complex and rolled out over time, creating uncertainty for steps 2 through 5. The handling of common subscription characteristics—e.g. evergreen subscriptions, nonrefundable upfront fees—becomes problematic as companies must decide whether to recognize revenue right away or defer it. Similarly, usage-based pricing can make determination of the transaction price (step 3) more complicated than before. This all adds to the difficulty of accurately tracking contracted, recognized, and unbilled deferred revenue.

What are the effects on growth?

For subscription-based companies, the new standards could impact growth by hindering sales and marketing efforts. In order to achieve compliance, businesses may feel forced to adjust their contract designs, pricing models, and practices for modifying and managing contracts. Companies might also feel obligated to change the way they forecast sales and manage their sales teams.

Take volume discounts as an example. Your hard-working sales team proposes a form of tiered pricing. The team strongly believes the initiative will bolster growth—a top objective for every business. When a customer subscribes for a certain number of seats, the price per seat is reduced, either for future additional seats, or retrospectively for the already-purchased seats.

But your finance department is nervous. Contracts would be modified on the fly—both prospectively and retrospectively—and prices would be continually changing, roiling all 5 steps of the revenue recognition model. Their manual process can’t scale up and be compliant at the same time. You’re forced to choose compliance over growth, vetoing the tiered pricing proposal.

Compliance doesn't have to be at the cost of growth

Subscription-based companies may instinctually resolve that growth-promoting marketing and sales initiatives must bend to compliance. But it doesn’t need to be this way. With the right technology, the decision isn’t binary.

The design principle we followed when building Zuora Revenue Management is “touchless revenue recognition.” How can we make sure that you, the user, has to worry about revenue recognition as little as possible - let us handle the complexity for you. Revenue management in Zuora is automated and aligned with your other finance applications. That's right, no more spreadsheets. It takes 3 simple steps:

- Design a set of rules for how you want to recognize revenue (including revenue distribution rules, performance obligation grouping rules, and more)

- Assign these rules to each of your offerings.

- Let Zuora do the work for you and watch revenue contracts, performance obligations, allocations, and revenue distribution happen automatically.

For companies who may have more volume or a higher level of complexity, RevPro is a great option to consider. RevPro is the industry-leading revenue recognition automation solution from our partners at Leeyo Software. RevPro integrates with Zuora, either natively or through middleware systems.

Regardless of your chosen solution, don’t let your systems hold back your growth strategies.

"

["post_title"]=>

string(83) "ASC 606 & IFRS 15: How the new Revenue Standards will Impact Subscription Companies"

["post_excerpt"]=>

string(0) ""

["post_status"]=>

string(7) "publish"

["comment_status"]=>

string(4) "open"

["ping_status"]=>

string(6) "closed"

["post_password"]=>

string(0) ""

["post_name"]=>

string(80) "asc-606-ifrs-15-how-the-new-revenue-standards-will-impact-subscription-companies"

["to_ping"]=>

string(0) ""

["pinged"]=>

string(0) ""

["post_modified"]=>

string(19) "2024-01-29 17:37:31"

["post_modified_gmt"]=>

string(19) "2024-01-30 01:37:31"

["post_content_filtered"]=>

string(0) ""

["post_parent"]=>

int(0)

["guid"]=>

string(128) "https://zuorainternprd.wpengine.com/2017/03/30/asc-606-ifrs-15-how-the-new-revenue-standards-will-impact-subscription-companies/"

["menu_order"]=>

int(0)

["post_type"]=>

string(4) "post"

["post_mime_type"]=>

string(0) ""

["comment_count"]=>

string(1) "0"

["filter"]=>

string(3) "raw"

}

[1]=>

object(WP_Post)#10856 (24) {

["ID"]=>

int(41597)

["post_author"]=>

string(2) "64"

["post_date"]=>

string(19) "2017-03-28 17:36:00"

["post_date_gmt"]=>

string(19) "2017-03-29 00:36:00"

["post_content"]=>

string(2261) "

Do you subscribe to the theory that change is good?

Ehhh, 'yes,' 'no,' or even a 'depends on my mood,' any answer is fine with us. We're simply wedging in use of the word 'subscribe' to highlight our recent article in partnership with our friends - and frequent collaborators - at Zuora for FEI Daily on some key changes coming down the pike for subscription-based businesses to consider.

Everyone can expect impact in some fashion from the impending new revenue recognition guidance, but businesses built on a subscription model will be hit more than most. New challenges in the form of new data requirements, pricing structures, price billing models and accounting needs are mounting for these businesses dedicated to long-term customer relationships rather than one-time transactions in isolation.

"Quite often, prior to the formal assessment, there is a false perception (particularly by the private companies) that the impact of the new revenue standards may not be material enough to justify the sense of urgency in dealing with it," said Peush Patel, Zuora's Product Management Director, on why so many firms remain stuck in early phases of new guidance adoption. "But once these subscription businesses perform the full assessment, they realize that certain business processes and the related IT applications need to be revised to ensure continuous compliance."

In the piece, penned jointly by Patel and Jagan Reddy, Leeyo's Co-founder, CEO and CTO, and titled "

The Top Five Changes in ASC 606/IFRS 15 for Subscription-Based Businesses," the duo swiftly boil things down to a manageable number for consideration, including - but not limited - to:

- The definition of a performance obligation

- Usage-based pricing

- Subscription amendments

Check out

the full article to learn more on these and other items well worth your consideration.

"

["post_title"]=>

string(61) "ASC 606 / IFRS 15 Changes Aplenty for Subscription Businesses"

["post_excerpt"]=>

string(0) ""

["post_status"]=>

string(7) "publish"

["comment_status"]=>

string(4) "open"

["ping_status"]=>

string(6) "closed"

["post_password"]=>

string(0) ""

["post_name"]=>

string(59) "asc-606-ifrs-15-changes-aplenty-for-subscription-businesses"

["to_ping"]=>

string(0) ""

["pinged"]=>

string(0) ""

["post_modified"]=>

string(19) "2024-01-29 17:37:30"

["post_modified_gmt"]=>

string(19) "2024-01-30 01:37:30"

["post_content_filtered"]=>

string(0) ""

["post_parent"]=>

int(0)

["guid"]=>

string(107) "https://zuorainternprd.wpengine.com/2017/03/28/asc-606-ifrs-15-changes-aplenty-for-subscription-businesses/"

["menu_order"]=>

int(0)

["post_type"]=>

string(4) "post"

["post_mime_type"]=>

string(0) ""

["comment_count"]=>

string(1) "0"

["filter"]=>

string(3) "raw"

}

[2]=>

object(WP_Post)#10868 (24) {

["ID"]=>

int(43938)

["post_author"]=>

string(3) "227"

["post_date"]=>

string(19) "2017-09-20 12:55:04"

["post_date_gmt"]=>

string(19) "2017-09-20 19:55:04"

["post_content"]=>

string(10616) "

This story was originally published in Accounting Today by Editor in Chief Michael Cohn.

The revenue recognition standard that takes effect in December for public companies could pose challenges for technology businesses, particularly those relying on traditional subscription licenses, and many companies aren’t ready for the impact on their financials.

“Revenue recognition feels like a big, big issue,” said

Zuora CEO Tien Tzuo, whose company specializes in software for managing subscriptions. “This feels as big or bigger than Y2K or SOX. SOX was a big heavy cost, but it wasn’t like you were in danger of missing your earnings call, or you had to report earnings that differed from expectations, not because anything changed in your business but because of accounting standards. We should be a little worried. There’s a surprise looming when earnings season kicks off at the start of next year and I don’t think we’re ready for it.”

He believes the Financial Accounting Standards Board isn’t taking into account the changing software industry, which is moving increasingly to the cloud, in the revenue recognition standard, also known as ASC 606.

“More and more of the real information is flowing out of the GAAP financials and into either footnotes or non-GAAP financials,” said Tzuo during an interview at Zuora's Subscribed conference in New York last week. “You’re back to the world where it’s harder to compare apples to apples, one financial statement to another. Instead of actually creating the rules, [FASB] seems to have gone the other way. They seem to say, look, we’re going to have this concept called deliverability of the contract. Did you deliver on what you contracted for? But we’re not going to define it. We’re going to let every company define it, and they’re just going to have to disclose how they do it with sufficient information in their filings. And that’s not really good. So we’re actually creating more ambiguity. We’re putting more judgment back into the hands of the CFO and CEO, so we actually think in talking to companies that these new ASC 606 rules are going to be a big step back. I think the intention is right, but the actual implementation has been a bit off base.”

The revenue recognition standard is also referred to as ASC 606, short for Topic 606 in the Accounting Standards Codification. But Tzuo suggested it might get more attention from companies if it had a catchier name.

“When we say things like ASC 606, the problem is you just don’t have an Enron, a Y2K,” he said. “ASC 606? I don’t know what you’re saying. We’ve got to give this thing a sexier name. It should be called ASC 666.”

Christoph Hütten, chief accounting officer at SAP, helped the International Accounting Standards Board develop its version of the revenue recognition standard under International Financial Reporting Standards, IFRS 15, which is mostly converged with ASC 606. “I think it’s more of a management, if not a cultural change, than an accounting change,” he said. “In SAP and a lot of our peers, revenue recognition in a lot of scenarios is a gatekeeper for good business. Everyone in sales and other functions look at revenue because they know that’s driving their compensation and commissions. That’s why they try to structure deals in a way that they are favorable from a revenue recognition perspective. And a lot of them have quite some expertise meanwhile in revenue recognition. Lots of companies tend to have structures of revenue recognition experts in the back who support them.”

He pointed out that SAP has separate accounting and revenue recognition guidelines. “Our accounting guideline covering everything beyond revenue recognition is about 500 to 600 pages,” said Hütten. “Our revenue recognition guideline is 700 pages. So the topic of revenue alone covers more pages in our guide than all other topics in accounting together. That’s to give you an idea of how important revenue recognition is for the company. And now somehow the rules of the game change. They’ve changed in a way that we have certain transactions that may have been unfavorable from a revenue recognition [standpoint] in the past that suddenly now get favorable revenue treatment. For some of those, people applaud—‘in a way we always wanted to do that and now finally we can and it’s great for the company.’ For some others you may think, well, we were happy in the past that we had revenue recognition as a gatekeeper. That helped prevent such business practices. Now revenue recognition moves out of the gatekeeper role, and now the question is what do we do with that vacancy? How do we fill this gatekeeper through something other than the revenue recognition rules?”

Zuora’s Tzuo believes many companies are unprepared for the changes that will be necessary. “A lot of companies were blindsided by this,” said Tzuo. “I think this has really caught them by surprise. It just doesn’t look like FASB spent a lot of time listening, especially to what I would say the growth sectors are in our economy, which is tech. It feels like a lot of these rules are based on old-school construction service contracts where they’re paying me over a three-year period to build a gigantic building or a retail complex, and it’s not based on this new world of services. There are services we can tap into on our phones and that we can pay for on an ongoing basis.”

With the revenue recognition standard, FASB and the IASB aimed to eliminate much of the industry-specific guidance that existed under the old accounting standards, making it more principles-based as opposed to rules-based.

“I think the goal is good, based on the fact that more and more of our economy is not shipping products, referring to the fact that we want some rules that can transcend industries versus something that’s too complex, with different rules for different industries, recognizing that we want some kind of harmonization between U.S. and European laws,” said Tzuo. “All of that is really, really good, but I think when you look at the implementation, there’s just a lot of silly things. There’s an arbitrary thing about commissions being over five years. Why five years? There are things too about selling a term license on a piece of software. If it was a three-year contract, I used to have to recognize the revenue over three years. The industry finally moved to some level of standardization, and now the rules say you’ve got to recognize the whole thing upfront. We’re back into that world that we tried to move away from. If you sell a five-year contract and I sell a three-year contract, it’s the same product, and the customers are paying on an annual basis, so why should you recognize more revenue than me? It’s going to encourage you to go and do longer-term contracts at a bigger discount, so you book more revenue this quarter, but you’re really just sacrificing your future revenue. All these things we tried to get away from, and it’s only going to slide back.”

At SAP, Hütten believes that revenue recognition for software subscriptions will differ somewhat for various types of products. “I think it depends a little bit on what you’re selling to the customer,” he said. “I think if it is a clear pure cloud subscription, and truly a cloud subscription, where the customer doesn’t install the software on the customer’s server, but it’s installed on the vendor’s server and the customer only accesses it, it’s really a service. For those, I don’t see significant changes over the plain vanilla where the customer pays a fixed fee for a certain period and gets the right to access. The challenge is more in the area where people sell either on-premise subscriptions or hybrid subscriptions, so the customer still installs the software, but rather than in the past buying the software once for a perpetual license one-time fee, it’s now a recurring fee. There are a number of software companies who have moved from that old model of a one-time purchase to this subscription model. With these licenses, even if the customer pays on a subscription basis, revenue will be recognized upfront under certain criteria. You will see companies that have moved over from a one-time event revenue recognition, one-sale software license revenue model over the last few years and moved into a subscription model and got applause for it from the capital markets. They now are challenged they’ll be pulled back into our old world of recognizing revenue upfront again for the entire contract fee because it is in the end not a cloud subscription, but a term license, and term licenses are now recognized upfront where they were under certain circumstances recognized over time.”

That could be a challenge for investors and capital markets, according to Hütten. “You can imagine if a company that has just walked through that change, going from upfront recognition to a range of recognition and got applause from the capital markets, to now go back to back to the capital markets and say, ‘Sorry, I’m back where I was. The business model hasn’t changed. The customers still have subscriptions, but unfortunately the accounting pushes me back to recognizing them upfront.’ That will be a difficult story to sell. I don’t know whether it will affect their business, but at least it will be from an investor relations and capital markets perspective a difficult story to tell. It’s not really a challenge for us because we’ve never been heavily in this term license business. I know some other companies who do, but it’s not for us. But I know it is for a number of other software companies.”

Public companies won’t have any choice but to adopt the new standard by early next year, though. “I think it is what it is for now,” said Tzuo. “Companies are going to rush to adopt it. There’s too much interpretation, too much judgment. Most companies will be OK, but I think there will be some high-profile disasters where there will be some misunderstanding or somebody will miss or delay their release of earnings and the stock prices are going to drop. Hopefully a year or two from now, we’ll normalize it to a different place and we’ll start advancing the ball again.”"

["post_title"]=>

string(64) "ASC 606 or 666? Revenue recognition standard could spell trouble"

["post_excerpt"]=>

string(0) ""

["post_status"]=>

string(7) "publish"

["comment_status"]=>

string(4) "open"

["ping_status"]=>

string(6) "closed"

["post_password"]=>

string(0) ""

["post_name"]=>

string(54) "asc-606-666-revenue-recognition-standard-spell-trouble"

["to_ping"]=>

string(0) ""

["pinged"]=>

string(0) ""

["post_modified"]=>

string(19) "2024-01-29 17:38:40"

["post_modified_gmt"]=>

string(19) "2024-01-30 01:38:40"

["post_content_filtered"]=>

string(0) ""

["post_parent"]=>

int(0)

["guid"]=>

string(44) "https://zuorainternprd.wpengine.com/?p=43938"

["menu_order"]=>

int(0)

["post_type"]=>

string(4) "post"

["post_mime_type"]=>

string(0) ""

["comment_count"]=>

string(1) "0"

["filter"]=>

string(3) "raw"

}

}

["list_grid"]=>

array(2) {

["section_title"]=>

string(0) ""

["list_items"]=>

bool(false)

}

}