By Amy Konary, Chair of the Subscribed Institute at Zuora

As I prepare for my trip to CES 2020 this week, I’m drawn to headlines about new innovations from the media industry. A hotbed for streaming and gaming, new services will no doubt be launched and existing ones amped up at CES this year. In fact, two of the eight keynotes are being headlined by streaming services—Quibi, a star-studded mobile subscription service for short-form video, and NBC Universal which is expected to focus on its Peacock streaming service, both of which are slated to launch in April.

With more than a hundred streaming services in the market and so many more on their way, I can’t help but wonder how many of them will still be around for CES 2025?

The conventional view will say that it depends on their ability to generate hit content. If these services are able to deliver a hit show once a year, that should guarantee their success, right? Not quite. Traditionally, success in the entertainment industry hinged on selling a mega-hit show to many different customers. But a successful Direct-to-Consumer (D2C) streaming subscription play relies on offering ongoing value to individuals and creating frictionless opportunities for them to find and consume different types of content. Hits might entice subscribers to sign up, but once the series is over, what gets them to stay?

Successful streaming companies focus on stickiness, not ratings. Since “value” is in the eye of the subscriber, providers must offer a broad range of content that both entertains and is easy to consume. According to a recent survey by KPMG, while content is still king, price, ease of access, and an ad-free environment are important considerations for streaming service subscribers.

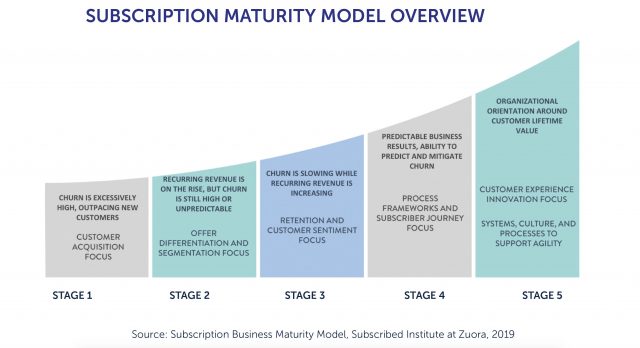

Getting all of this right isn’t easy. And most media streaming companies sit somewhere within the five stages of subscription maturity.

Stage 1

The focus in Stage 1 of subscriptions is on signing up new subscribers above all else, not on keeping them. With no focus on retention outside of creating new hit offerings, the customer experience is inconsistent and churn is typically high. According to Zuora’s latest Subscription Economy Index, the average churn rate for B2C companies was 24% last year. Wild West companies see rates far exceeding that.

Stage 2

Here, companies begin to build efficiencies that reduce acquisition costs, such as making it easier for new subscribers to sign up in low- touch ways, as well as on service scalability. At this stage, it might be attractive to build relationships with an aggregator such as Apple that can offer scale and reach. However, in exchange, the provider gives up the direct relationship with the customer, as well as control over service and subscriber usage data.

Stage 3

In this stage, there begins to be a strategic focus on retaining subscribers. In the video streaming business, doing so requires compelling and differentiated content. But it also means making it easy to find and consume this content. Structures are put in place to optimize the renewal process, and the concept of a subscriber journey or lifecycle is taking shape.

Stage 4

Companies at this stage have not only developed and articulated customer journeys but are also using data to help manage and drive all aspects of the business. This is why Smart TVs that include the Netflix app must agree to terms that prohibit them from capturing audience data. Customer data is gold in the subscription model. Content providers that are trying to build subscription businesses through aggregators must protect access to service usage data and subscriber preferences to progress to this level of subscription business maturity.

Companies in this stage also offer subscription agility, such as the ability for customers to pause, cancel, or resume services, as well as easily add services or change service tiers. Trust is now a core value and an essential component for moving to Stage 5.

Stage 5

In an optimized subscription business, suppliers and their customers work together to achieve outcomes. There is a clear and systemized cadence of customer contacts focused on building and deepening relationships. A sign of an optimized subscription business: while they continue to sign up new subscribers, a large portion of recurring revenue comes from increasing value (and price) for existing subscribers.

Companies offering digital subscription services must continually ask themselves—What are subscribers coming to us for? And what will make them stay long after the series is over? With this North Star vision in mind, streaming service companies should assess where they are in their subscription business maturity and work towards progressing to the next stage.

With many of the traditional media companies switching to streaming and new services entering the space, it will be interesting to see how streaming companies deal with the competition.

The good news is that there’s a healthy appetite for new services amongst consumers. The KPMG survey also found that while there’s a high degree of price sensitivity around streaming services, there’s a willingness to spend. On average, survey respondents pay $22/month for video streaming services and are willing to pay an average of an additional $11 more. That’s 50% more for additional services.

There’s no doubt that converting a large percentage of new consumers into long-term subscribers will require a combination of hit content, sticky services, and subscription business maturity. Here’s hoping that many of these streaming companies will be able to capture that market and be back at CES 2025!

If you’ll be at CES this year, please join me at Subscribed at CES, where I will be presenting the keynote and speaking with Sara Carlson, Partner, Industrial Sector Connected Car GTM at IBM, and Matthew Vernardi, GM, Kinto Link at Toyota about building consumer-centric technology companies. I’d love to see you there!