This story was originally written by Daren Fonda and published on the cover of Barron’s on May 6, 2019 titled, “5 Stocks to Ride the Coming Wave of Millennial Spending”.

“The store is just sick.”

Oscar Quinones, 28, was in Nike ’s flagship store on Fifth Avenue in Manhattan, and he was speaking out of reverence, not disgust. The store has a design studio on the top floor where experts dole out advice on fit and fabrics and how to use Nike gear.

“I walk in and see all the parts of the shoes, how they’re made, and how Nike comes up with their designs,” Quinones, a nursing student from the Bronx, told Barron’s. He was there to pick up his 17th pair of Nikes, the first ones he had designed and customized online: a glow-in-the-dark Kobe A.D. sneaker with the initials OQ stitched on the heels.

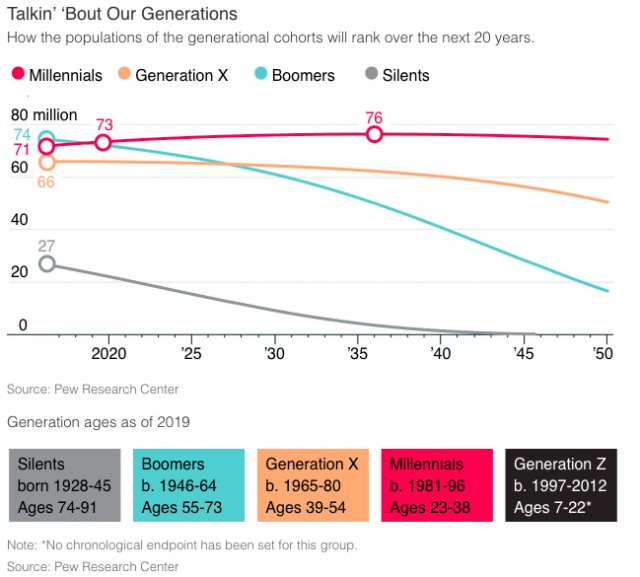

Millennials like Quinones are being aggressively wooed by Nike (ticker: NKE) and other marketers, and for good reason. The millennial generation, consumers in their mid-20s and 30s, is overtaking the baby boomers as the largest generation of shoppers in history. By 2020, millennial spending will account for $1.4 trillion in U.S. retail sales, according to the consulting firm Accenture . That will be a quarter of the estimated $5.7 trillion total, according to eMarketer.

This year, the oldest millennials are turning 38—a prime age for young families and household formation. Spending tends to rise with income as consumers reach their late 30s and 40s, and then tapers off in their 50s, according to Census Bureau data. The youngest millennials, in their early 20s, are finishing up college and graduate school and are entering the workforce at a time when jobs are plentiful and demand for young workers is the strongest in years.

The maturing of the millennials will lift spending for all sorts of industries and companies—a powerful demographic tide that should continue rising as the population grows and workers enter their prime earning years.

“Clearly, one would expect millennial spending to increase healthily over the next decade or so,” says Richard Fry, a senior researcher with the Pew Research Center.

The demographic changes aren’t all positive. Baby boomers are spending less as they age into retirement and live off their savings, and Gen X consumers in their 40s and 50s aren’t as large of a generation, creating a consumption gap.

Millennials will eventually pick up the slack as their incomes rise, but it won’t happen overnight. In the meantime, investors should seek the industries and companies with “niche demographic tailwinds,” says Pat Tschosik, an analyst who studies demographic trends with investment-research firm Ned Davis Research. Companies that can benefit from millennial demand—that isn’t offset by declines from the boomers or Gen Xers—are in the demographic sweet spot.

How do investors take advantage of these shifts?

One could invest in companies whose growth is being fueled by millennial spending, but that is a scattershot approach to what is a vast universe. Companies as different as Amazon.com (AMZN) and General Motors (GM) get pitched as investments because of “secular” demand by millennials.

Some exchange-traded funds bundle it all together. The Global X Millennials Thematic ETF (MILN) holds about 80 stocks that have a “high likelihood of benefiting from the rising spending power and unique preferences” of millennials. It consists of companies like Alphabet (GOOGL), Costco Wholesale (COST), Facebook (FB), Starbucks (SBUX), and Walt Disney (DIS). Another ETF, Principal Millennials Index (GENY), holds a basket of global growth companies, including an Australian education business, Navitas (NVT.Australia), the Japanese retail giant Fast Retailing (9983.Japan), and Chinese internet stocks Alibaba Group Holding (BABA) and Tencent Holdings (TCEHY).

While millennials certainly matter to these companies, they are hardly the only drivers of the stocks. Valuations, competitive pressures, and earnings are likely to be as influential as a generational shift in spending.

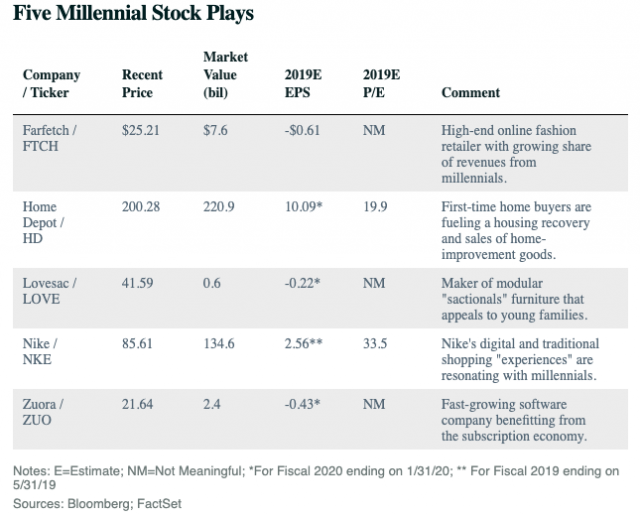

Barron’s has identified five stocks that should benefit from millennial spending and are attractive for other reasons, as well. Here are our millennial plays, two well-known big names and three smaller, more speculative picks:

Subscription services, as Barron’s highlighted in a December cover story, are thriving. Millennials aren’t the only ones behind the trend. But plenty of research indicates that young people prefer to rent products and services more than older generations. According to Accenture, 77% of both the millennial and Gen Z generations say they are interested in curated subscriptions to products or services. Legions of companies are now adopting subscription-revenue models for products as varied as furniture (IKEA) and electric-toothbrush heads (Philips).

That’s the opportunity for Zuora (ZUO), a small but fast-growing software company. Zuora sells a cloud-based platform to handle back-office functions for subscriptions, such as billing, revenue recognition, and analytics.

Its customers include auto makers GM, Ford Motor (F), Kia Motors(000270.South Korea), and Toyota Motor (TM); HBO Go (the direct-to-consumer service); office-productivity company Box (BOX); and Caterpillar(CAT).

Caterpillar’s mining earth movers, for instance, are operated remotely with GPS and robotics. Companies pay subscription-based fees for maintenance and upgrades of the equipment, and the company uses Zuora to handle its subscription revenue. Trucking companies are also using subscription software to keep track of hours and miles driven, with Zuora as the go-between.

The idea is to “sign up new customers, increase spending per customer, benefit from increased customer usage, and retain as many of those customers as possible,” says David Meier, a portfolio manager with Motley Fool Asset Management, which owns Zuora in the MFAM Small-Cap Growth ETF (MFMS).

Zuora’s sales are expected to reach $292 million in its fiscal year ending in January 2020 from $235 million in fiscal 2019. Analysts expect the company to lose 43 cents a share this fiscal year. Yet the losses are narrowing as revenue increases and cash flows cover more of its operating expenses. The company has more than enough cash on its balance sheet, at about $180 million, to sustain the business for several years without another equity issuance.

“This is a growth story,” says Scott Berg, an analyst with Needham who has a Strong Buy rating on the stock with a $30 price target from a recent $21.50. “They’re targeting investment over profitability near term.”

Zuora’s end market will be one of the fastest-growing in enterprise software over the next five years, he says, expanding at a 25% annualized rate. Its revenue should grow at roughly that rate, Berg estimates. The valuation looks reasonable, with the stock trading at 5.8 times enterprise value to sales, slightly below the median for software-as-a-service companies.

Zuora CEO Tien Tzuo tells Barron’s that profitability isn’t the company’s near-term priority. “We see this is a long-term game,” he says. In the auto industry, he says, subscription models and car-sharing will be far more prevalent a decade from now, requiring subscription software to handle the billing and other tasks. He also sees growth for subscription software with the rise of connected devices like internet-enabled thermostats and the broader Internet of Things.

Subscription-based revenue models are growing at five times the pace of the average S&P 500 index company, he says. If he is proved right, Zuora’s stock could double over the next five years.

Whether or not luxury department stores survive, millennials are likely to buy more luxury goods online. By 2025, 25% of luxury items will be bought online, up from 10% in 2018, says the consulting firm Bain & Co. Much of that growth will be driven by millennials and Gen Z, who will account for 45% of total luxury sales, up from 32% in 2017.

Farfetch (FTCH) aims to profit from the spending wave. An online platform for luxury brands, the site is a mash-up of fashion magazine and high-end boutique. Shoppers can browse hundreds of brands or buy the style “edit” of celebrities like Chloë Sevigny, who recently showcased a Gucci tweed coat ($4,980) and Miu Miu leopard-print trench coat ($3,650).

Fashion is a globally inefficient industry: Small boutiques and brands in Europe, Japan, and other regions handle cross-border sales, shipping, and inventory management in small batches. Farfetch provides all of that on a global scale, including same-day delivery in 18 global cities. Luxury brands work with Farfetch because it gives them control of listings, allowing them to maintain pricing and “consumer perception,” Oppenheimer analyst Jason Helfstein wrote in a recent report.

Farfetch is gaining traction. The total value of merchandise on the site reached $1.4 billion in 2018, up from $910 million in 2017. Active users climbed to 1.35 million from 936,000. Farfetch has also been acquisitive, buying a Chinese luxury platform from JD.com (JD) and a premium sneaker and streetwear marketplace, Stadium Goods.

Farfetch went public in September at an initial price of $20 and trades around $25. Company insiders own more than a third of the shares, and the stock could face selling pressure after the lockup period, which expired on March 21. Other risks include a slowdown in sales in the Middle East and Asia-Pacific, fast-growing regions for the company. Analysts expect the company to lose 61 cents a share in 2019 and 45 cents per share in 2020. The shares trade at about 11 times sales, a 50% premium to the industry, according to FactSet.

But Farfetch has no debt on its balance sheet, $850 million in cash on hand, and minimal inventory. Sales are expected to increase 30%, to $1.1 billion in 2020 from $822 million this year. Helfstein estimates that Farfetch will turn a modest profit of $20 million in 2022, based on adjusted earnings before interest, taxes, depreciation, and amortization.

The business looks defensible against Amazon.com, says T. Rowe Price fund manager Jay Nogueira. “The high-end brands don’t want to be on Amazon,” he says. “The addressable market for Farfetch is massive, and platform companies like this will be winners.”

Housing should get a boost as millennials form households and have children.

Millenials have moved out of their parents’ homes (with 85% no longer living at home). And they appear to be buying after years of renting; owner-occupied households increased to 64.8% in late 2018 from 62.9% in early 2016, while renter-occupied households dipped by 1.9 percentage points, according to the Census Bureau. Tschosik estimates that there is pent-up demand of at least two million housing units by millennials who had delayed buying because of the recession and weak job market.

Home builders targeting first-time buyers, such as KB Home (KBH), should see some benefits from this wave. But first-time buyers are more likely to purchase older homes; new construction tends to be more expensive, and the average age of a new-home buyer is 47, making a new house more of a trade-up.

That should benefit Home Depot (HD), as millennials buy older homes and fix them up. Household spending on home improvement tends to be highest in the first couple of years of ownership. And in a strong economy, with wages and home prices on the rise, discretionary budgets should be healthy enough to support spending on remodeling.

Home Depot’s stock has lagged behind the broader market over the past year, gaining about 8%. Wall Street’s sentiment on the stock has soured a bit as the housing market weakened and the company missed estimates for same-store growth in its last quarter. The stock trades at its average valuation over the past five years, about 20 times forward 12 months’ earnings.

Yet the retailer’s core sales trends still look healthy. The company expects same-store sales to increase 5% in 2019, similar to its growth rate in 2018. Spending on home improvement should continue to rise, especially if interest rates come down another notch.

Home Depot also has better locations than its chief rival Lowe’s (LOW), RBC analyst Scot Ciccarelli says. More of HD’s stores are located in dense urban areas, supporting higher foot traffic per store and stronger sales to professional contractors, one of HD’s faster-growing and higher-margin businesses.

Home Depot’s stores are also concentrated in areas with higher household incomes, all of which may give it a structural advantage over Lowe’s, Ciccarelli says. And Home Depot is investing heavily in e-commerce to fend off Amazon; the company is spending $1.2 billion over the next few years to expand distribution of big or bulky goods with same- or next-day delivery.

The stock isn’t likely to outperform if the macro climate for housing deteriorates. But the demographic elements look favorable, and there should still be upside in the stock if the company can execute on plans to improve same-store sales and margins. The stock yields 2.7% and the company recently authorized a $15 billion share-repurchase plan, equal to about 7% of its market value. Ciccarelli sees the stock reaching $223 over the next year, up from recent prices around $200, based on a multiple of 22 times estimated 2019 profits.

Families moving from apartments to houses tend to ramp up spending on home furnishings. That’s advantageous for Lovesac (LOVE), a small company that makes modular couches called “sactionals.”

Lovesac’s couches and other furniture can be reconfigured, accessorized, and customized into thousands of arrangements like interlocking Lego pieces. The cushions are made of recycled bottles—appealing to millennials who want sustainable products—and the furniture doesn’t have to be tossed in the landfill or sold on Craigslist as people move from apartments to larger living spaces.

“They’re a disruptive name in the furniture space,” says Brian Bythrow, portfolio manager of the Wasatch Micro-Cap Value fund (WAMVX), which owns the stock. Lovesac derives most of its sales from showrooms, online, and shops-in-shops within Costco. It has gross margins of 55%, well above rivals like RH (RH) at 40%.

Lovesac went public in June 2018 at $16 and now trades at $42. Analysts expect the company to lose 22 cents a share in the current fiscal year, which ends in January 2020 and earn seven cents a share in the next fiscal year. The stock trades at three times enterprise value to sales, well above average for furniture retailers.

Lovesac, however, is expanding rapidly. It is expected to report $239 million in fiscal-2020 sales, up 44% from fiscal 2019. The company is running at close to break-even because it is plowing revenue into expanding the business, Bythrow says. “We’re in a period where investors are rewarding companies that reinvest for growth,” he says. “That might change. But you can get by with that today.”

Nike’s appeal rests on spending assumptions by millennials, along with moves the company is making to refresh its product lineup and retail shopping experience. The company is deploying its vast financial resources to blend digital shopping with in-store experiences, says Jill Standish, head of retail for Accenture. “The Nike store experience is very Instagrammable,” she says.

The ability of consumers to design their own sneakers at kiosks at flagship stores is helping Nike fend off Amazon and other pure online retailers. Nike’s SNKRS app is also resonating with young shoppers, says Camilo Lyon, an analyst with Canaccord Genuity, and the company is doing a good job of driving sales through a combination of digital and in-store experiences.

“Nike is focused on driving the consumer experience across all components of their business,” he says.

Lyon points out that Nike’s innovation machine is cranking up; it includes the launch of a new cushioning platform in running shoes and a renewed focus on women’s apparel and footwear (such as its Air Max Dia shoe).

Nike also plans to drive innovation down from its upscale footwear to “core” sneakers priced below $100, an initiative that could take share from Under Armour (UA) and Skechers USA (SKX).

“Among the publicly traded companies, Nike has made the sharpest turn in strategy to address the millennial demographic and the changing landscape of shopping behavior,” Lyon says.

Nike stock, to be sure, looks pricey at 33 times earnings for the fiscal year ending in May, according to consensus estimates. That’s well above Nike’s five-year average price/earnings ratio of 23, and it is a steep premium to the market’s P/E of 17. Still, Lyon notes that Nike’s multiple has a history of expanding when profit growth is accelerating. Analysts expect year-over-year earnings growth to jump from 4.9% in fiscal 2019 to 19.2% in fiscal 2020.

The company’s latest quarterly results portray broad-based strength with sales up 11% (in unadjusted currency terms) over the prior year. The company is exhibiting price resiliency with gross margins up 1.3 percentage points, to 45.1%, driven by higher average selling prices and growth in direct-to-consumer sales.

Moreover, Nike is strong enough financially that it can afford to buy back a large amount of its stock. It just embarked on a four-year plan to repurchase $15 billion worth of shares, about 11% of its $134 billion market value. The stock has advanced 15% this year to $85.50, but Lyon sees further upside to $96 over the next 12 months.

That path will be made possible by customers like Quinones, who was picking up his sneakers at the Nike store in New York. He played around with the hundreds of color, material, and embroidery options in the Nike app before heading to the store to get his unique pair.

Visiting the store and seeing everything in action keeps him coming back. “It definitely makes me spend more money at Nike,” he says.